OkiMdp/iStock via Getty Images

If you are a hot dog fan, there’s a high probability that you are well aware of the Nathan’s Famous brand name. Well, it is more than just a brand name. The product itself is actually produced and sold by the company also known as Nathan’s Famous, Inc. (NASDAQ:NATH). Back in February of last year, very close to one year ago as of this writing, I found myself interested in whether or not Nathan’s Famous made for an attractive opportunity. In addition to being a high-quality player in its space with multiple revenue streams and a variety of other offerings that it sold such as sausage, corned beef products, and even frozen crinkle cut French fries, the enterprise had exhibited an increase in sales and a modest uptick in profitability in its latest fiscal year.

Unfortunately, all of these elements combined do not necessarily translate to an appealing opportunity. At the end of the day, value investing is about acquiring shares of a firm at an attractive price. Ideally, this would be at a price that is at a discount to the firm’s intrinsic value. And if you cannot get that, you should at least pay a price that is cheap relative to what the growth of the underlying firm is likely to achieve moving forward.

Based on my opinion back then, Nathan’s Famous did not meet either of these standards. The stock looked a bit pricey relative to its historical financial performance. This led me to rate the enterprise a “hold” to reflect my view that the shares of the firm would be likely to no better than match the returns of the broader market for the foreseeable future. Since then, the outcome has been a bit worse than I would have anticipated. While the S&P 500 (SP500) has jumped 14.2%, shares of Nathan’s Famous have seen downside of 2.9%.

The picture hasn’t changed enough

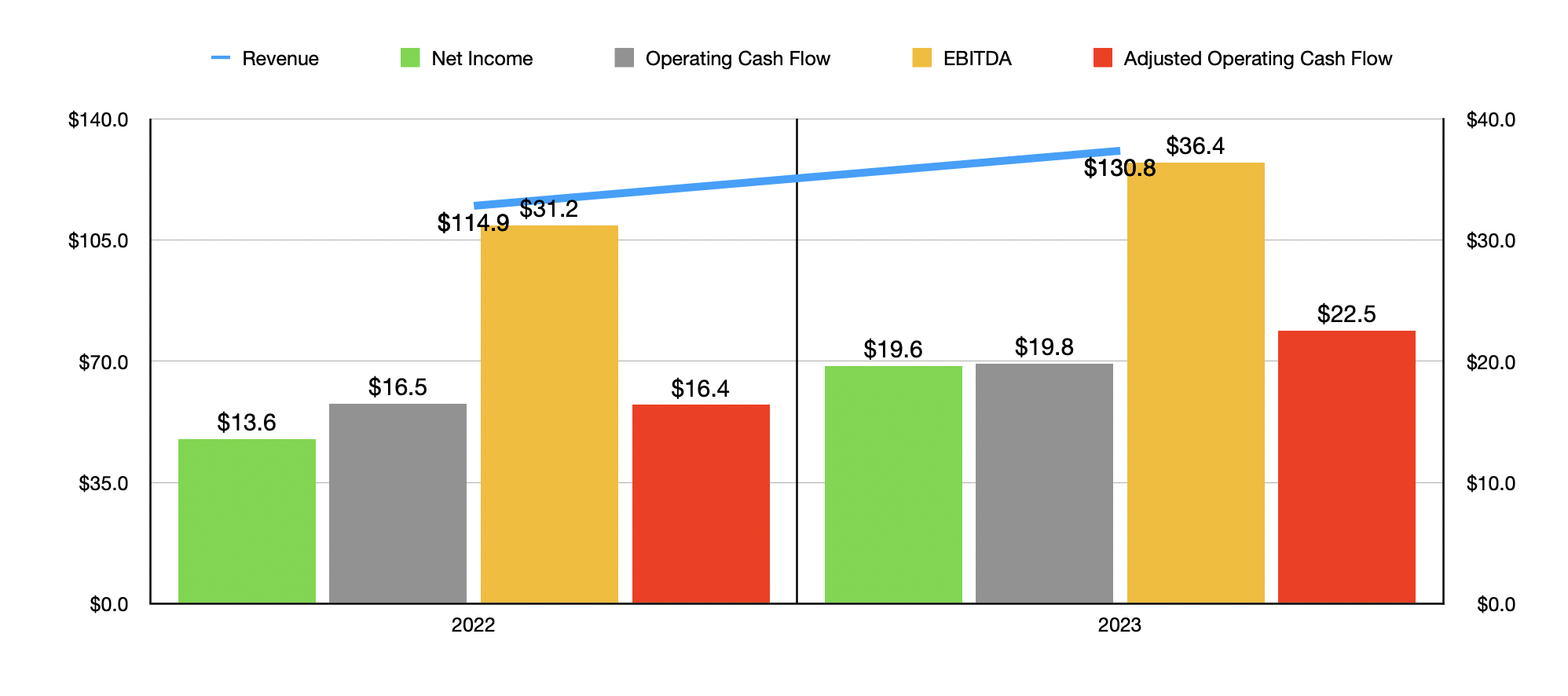

Truthfully, I want the financial performance of Nathan’s Famous to be worthy of an attractive rating. Those who followed the company’s financial performance through the end of the 2023 fiscal year might very well think that the company was well on its way to growth after years of stagnation. Even though the number of units in its franchise system dropped from 239 in 2022 to 232 in 2023, revenue for the business jumped from $114.9 million to $130.8 million.

That increase in sales, amounting to roughly 14%, was driven by multiple factors. A 15% rise in the volume of hot dogs sold under the firm’s Branded Product Program, combined with a 4% increase in average pricing for all of the company’s beef products combined, was instrumental in pushing revenue higher. The company also benefited from a 12% rise in revenue associated with its company-owned restaurants thanks to higher traffic at its Coney Island locations. There were other contributors as well, such as a 5% rise in revenue associated with licensed royalties and an 11% rise associated with franchise fees and royalties. But those are fairly small portions of the company’s overall revenue.

Author – SEC EDGAR Data

With this increase in sales, especially with the price component involved in the mix, profits jumped nicely, climbing from $13.6 million in 2022 to $19.6 million in 2023. Other profitability metrics followed suit without exception. Operating cash flow, for instance, expanded from $16.5 million to $19.8 million. If we adjust for changes in working capital, we get a rise from $16.4 million to $22.5 million. And lastly, there is EBITDA. That particular metric popped up from $31.2 million to $36.4 million.

Author – SEC EDGAR Data

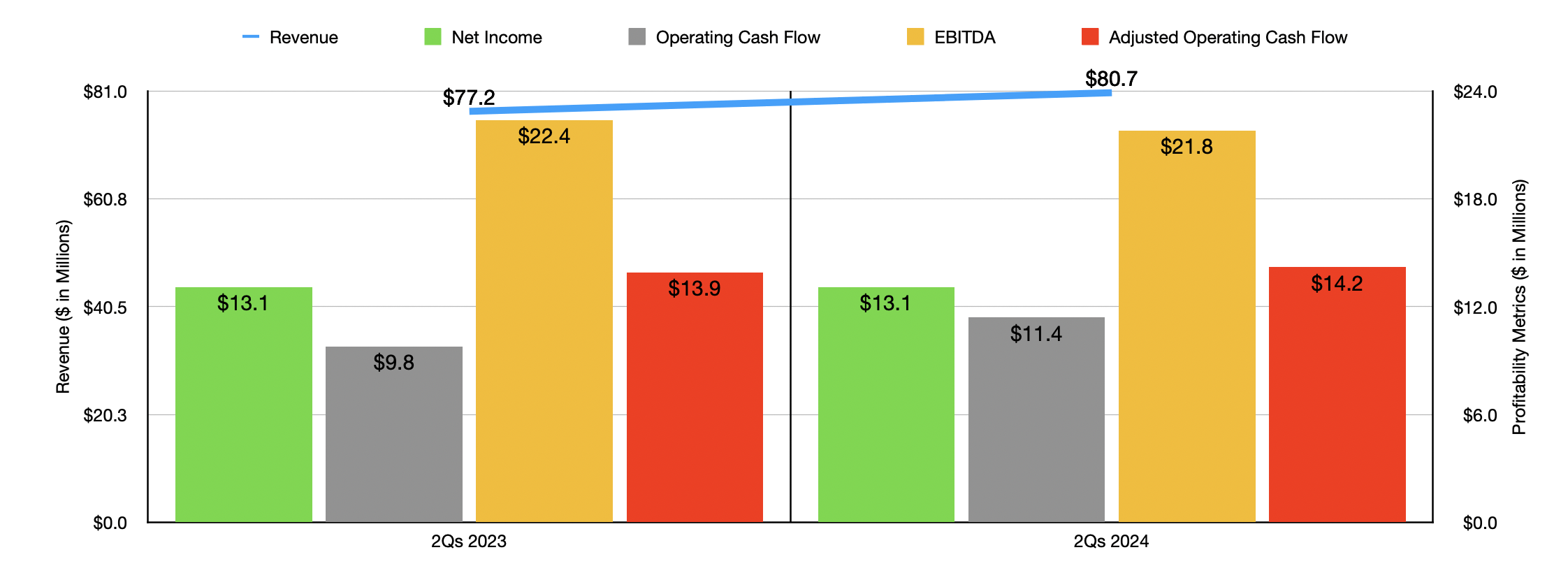

Unfortunately, the 2024 fiscal year has so far looked a bit different. The good news is that for the first two quarters of the 2024 fiscal year, sales have continued to climb, hitting $80.7 million compared to the $77.2 million reported the same time one year earlier. A 7% rise in average selling prices for the company’s beef products was the primary driver of the sales increase during this window of time. Volume was up only 0.4%, while the company saw weakness in some other areas. Most notably, company-owned restaurant sales actually fell 2% year-over-year because of reduced traffic caused by inclement weather.

You would think that an increase in sales would bring with it higher profits, especially when most of the rise in revenue was driven by higher average selling prices. Unfortunately, that was not the case. Net profits actually remained unchanged at $13.1 million year-over-year. A 12% increase in the average cost per pound of its hot dogs was partially responsible for this. The company also had other issues, such as increased operating costs at its restaurants.

This does not mean that all profitability metrics for the company failed to move higher. Operating cash flow actually fared quite well. It popped from $9.8 million to $11.4 million, while the adjusted figure for it expanded from $13.9 million to $14.2 million. The only profitability metric to worsen year-over-year was EBITDA. It fell from $22.4 million to $21.8 million.

Author – SEC EDGAR Data

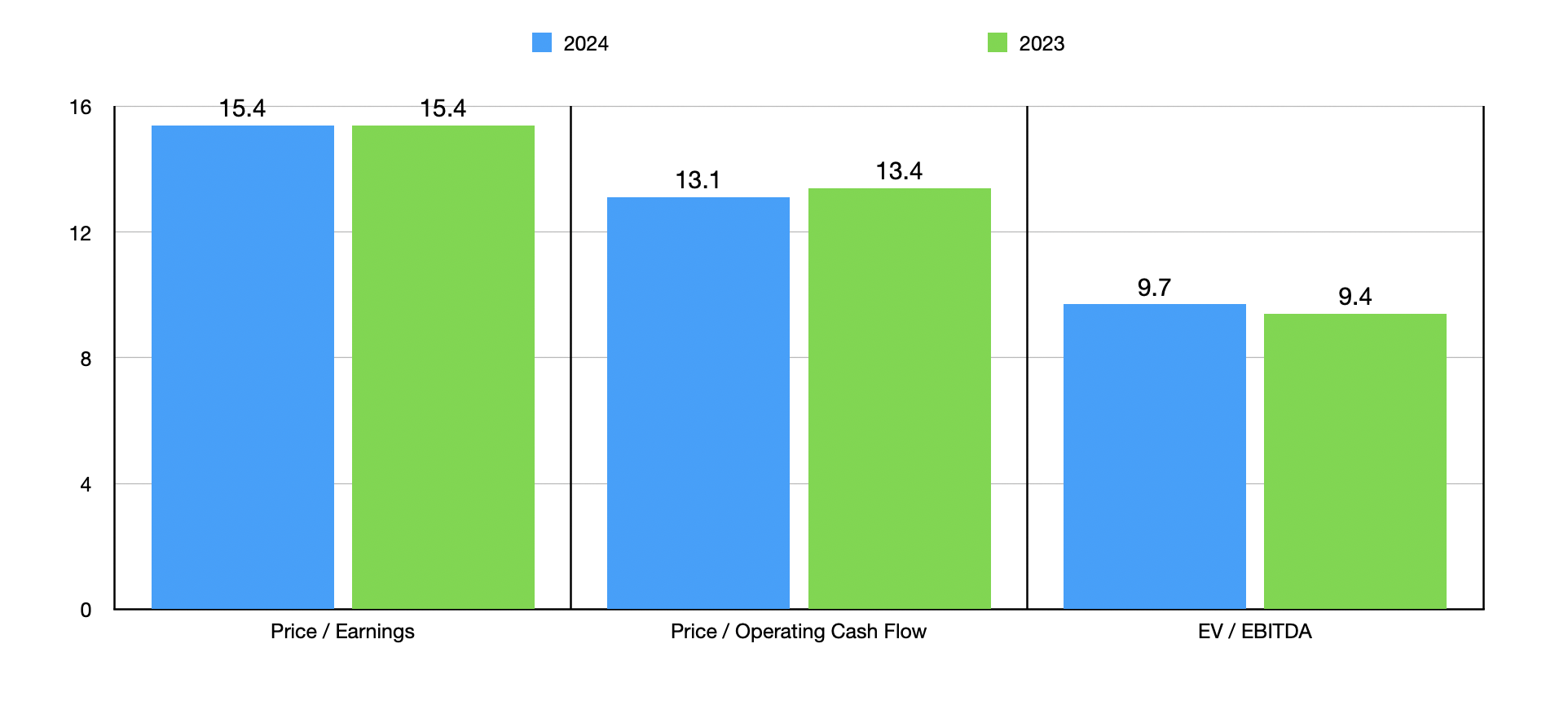

When it comes to the 2024 fiscal year in its entirety, it’s unclear what investors should anticipate. Based on how earnings have been so far, I would say it’s not unreasonable to expect an outcome very similar to what was seen in 2023. Based on my own estimates, I would say that adjusted operating cash flow should come in a bit higher at about $23 million this year, while EBITDA should be somewhere around $35.4 million. Using these estimates, I was able to value the company as shown in the chart above. I then, in the table below, compared the enterprise to five similar firms. On both a price to earnings approach and an EV to EBITDA approach, I found that only one of the five companies was cheaper than Nathan’s Famous. But using the price to operating cash flow approach, three of the five ended up being cheaper.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Nathan’s Famous | 15.4 | 13.1 | 9.7 |

| Hormel Foods (HRL) | 22.0 | 16.9 | 15.0 |

| General Mills (GIS) | 15.5 | 12.4 | 11.0 |

| McCormick & Company (MKC) | 27.6 | 17.2 | 19.4 |

| Tyson Foods (TSN) | 54.9 | 11.2 | 28.1 |

| Cal-Maine Foods (CALM) | 5.9 | 4.5 | 3.1 |

Takeaway

Although the 2023 fiscal year was quite solid for Nathan’s Famous, Inc., more recent data shows that, at least on the bottom line, the company still is only expanding at a very slow pace. The stock does not look particularly expensive, but it’s definitely not cheap enough, given the growth that we have seen, to warrant a great degree of optimism. If shares were to drop another 15% or 20%, I think I could bring myself around to rating it in a more bullish light. But until that occurs or fundamentals improve nicely, I still think that the “hold” rating I assigned the company is logical.

Q2 2024 Earnings Call Transcript")