Andrzej Rostek/iStock via Getty Images

The iShares J.P. Morgan USD Emerging Markets Bond ETF (EMB) isn’t exactly an exclusively emerging market ETF, but there is a fair bit of emerging market exposures indeed. We think the two factors are that the dollar should decline with trades unwinding at least a little and that inflation is more under control in emerging markets, where in a lot of cases inflation is much more benign and/or under control. We think there’s a decent case with EMB.

EMB Breakdown

The expense ratio is 0.39%, which is not too high considering the somewhat exotic nature of the portfolio, including both bond exposures and the foreign element. Duration is quite long at more than 7.2 years, and the YTM is at 7%.

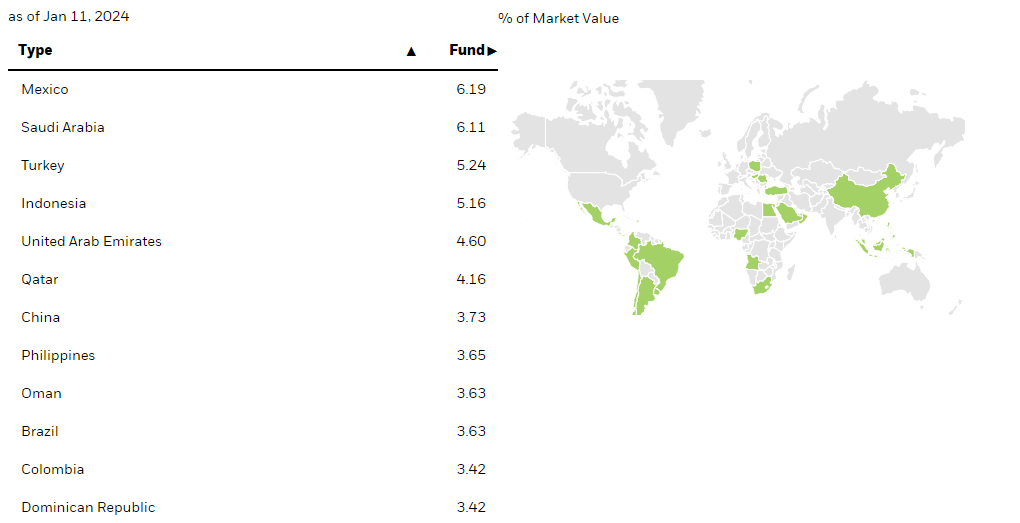

EMB Geography (iShares.com)

The geographic exposures are critical to consider as well. There’s quite a lot of Mexico at 6.2%, quite a lot of Gulf Nations, Turkey, and Indonesia and then quite a bit of South America led by Brazil. The full list is just above.

Comments

Let’s begin with a specific set of comments on Mexico since it features meaningfully in the mix of debt, mostly sovereign. Inflation is back to normalized levels, near 2019 levels at some points, and rates remain high. The MXP has implicit dollarization due to its trading relationships with the US and remittance dynamics. Inflation is at 4.8%, but quite a lot of that inflation is benign, coming from greater investment and appreciation of Mexican high-quality labor which remains undervalued. They have space for their higher rates, and the MXP has been growing with respect to the dollar on USD decline speculation after Powell’s comments. By the way, we wouldn’t call Mexico an emerging market.

While there are some perennially weaker spots like Turkey, in general, the reality is that many of the “emerging” markets feature similar dynamics. There is inflation, but it is benign and coming from general standard of living increases in these countries. They are also seeing currency benefits thanks to better market fundamentals and space for more restrictive policies with interest rates that were needed in 2022-2023 to deal with the initial bout of inflation coming from shocks that impacted global markets. Emerging markets tend to also have other economic motors like commodities that are at the fore currently, with the Gulf States being the best example, and there is quite a lot of exposure to Saudi Arabia, Qatar, the UAE, and Oman. Other exposures in the portfolio feature similar remittance dynamics, have valuable natural resources, or have other factors that put it at least in line with the dollar in terms of currency performance as well as in economic fundamentals.

This is all quite important as funds will be flushed back to the fringes of commodity markets as the dollar takes a back seat. While we have our doubts around the inflation campaign in the US, as we think it stays quite high, the Fed will have to deal with growth so rates will need to come down. More importantly, a failure to deal with inflation will also cause markets to eschew the dollar further, which provides an FX benefit to fixed income investments in emerging markets. Decent economic fundamentals in many of the “emerging” market countries, including oil-centered economies, all help keep spreads on the lower side too. Space for higher interest rates and benign inflation helps provide more options, including for lower rates which they may do as they can afford to do so while staying competitive with a lower-yielding dollar in the future. With the duration of the ETF, that duration effects should play nicely as well.

The duration is a bit of a concern as it interacts with general volatility in these economies, which don’t have the benefit of an established currency among other things. Also, the price has already made a rally to levels not too far off highs. On the other hand, space to reduce rates if the dollar becomes less competitive means a lot more growth could still be in store. In all, EMB is not a bad proposition, and you get quite an exotic exposure for the maintenance costs of 0.39%.

Q2 2024 Earnings Call Transcript")