Inflation continues to be sticky, which is posing significant challenges for companies with limited pricing power.

Unfortunately, I see evidence that my thesis of prolonged above-average inflation is still true, especially after the most recent inflation numbers.

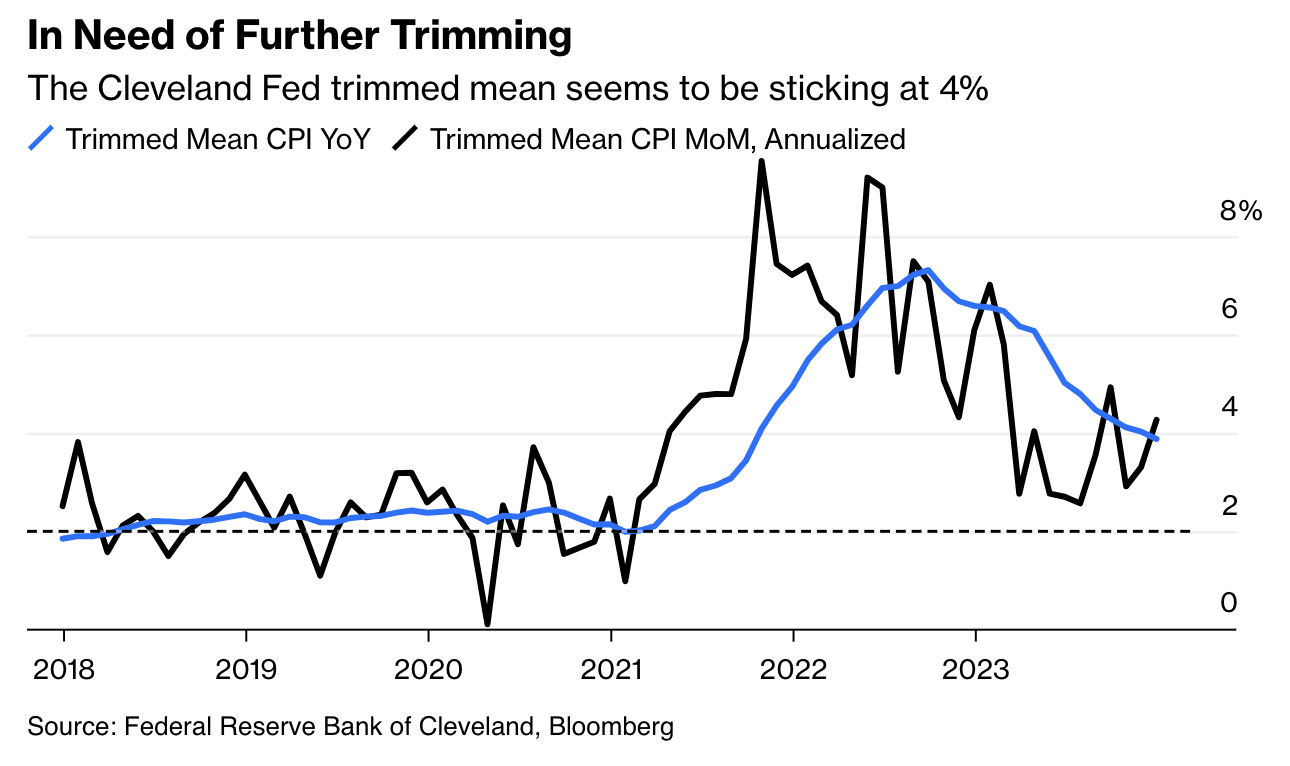

To use the worlds of Bloomberg’s John Authers (emphasis added):

The trimmed mean measure published by the Cleveland Fed is beloved by statisticians. It excludes the biggest outliers in either direction and takes the average of the rest for a good measure of core underlying inflation. On a year-on-year basis, disinflation continues but has become painfully slow. The month-on-month version has risen for the last two months, having hit a low last summer. This seems to confirm a picture of a disinflation which if not totally stalled or reversed is disappointingly slow:

Bloomberg

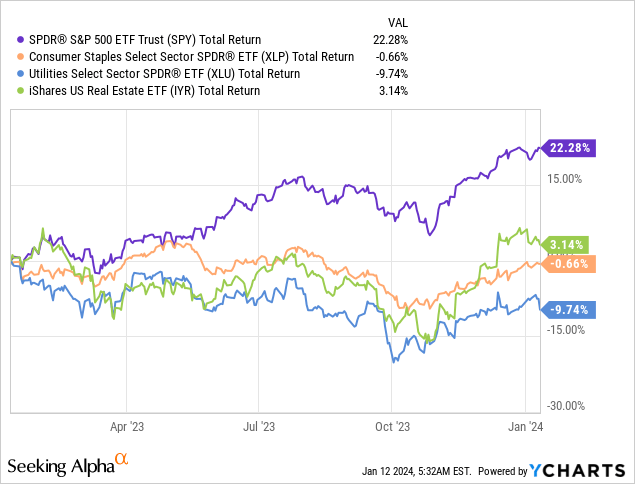

Companies suffering from elevated inflation are utilities, consumer staples, real estate companies, and similar companies with limited pricing power.

Over the past twelve months, all of these sectors have underperformed the S&P 500 by a huge margin.

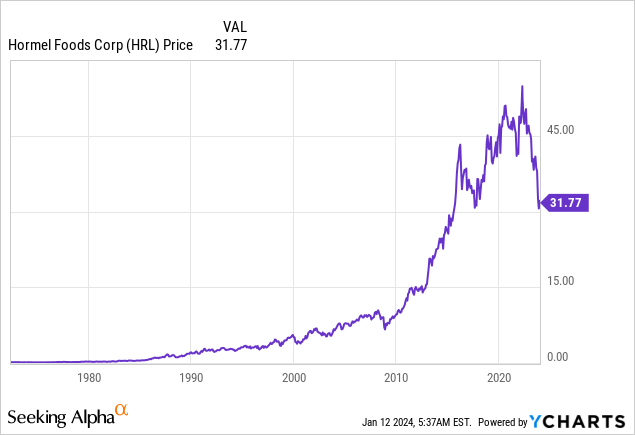

One of the worst performers in the consumer staples sector is Hormel Foods (NYSE:HRL), a company I most recently covered on May 31, when I wrote the following:

HRL maintains a healthy balance sheet, and analysts expect its free cash flow to grow, supporting the dividend and moderate future dividend growth.

While the current valuation is fair, HRL can be a suitable addition to a conservative dividend portfolio during periods of subdued inflation and healthy consumer sentiment.

Potential investors may consider starting small and averaging down, as there may be more room for the stock price to fall.

Room for more downside turned out to be true, as HRL shares are down 16% since then. The HRL ticker is now trading 40% below its all-time high, excluding dividends.

The good news is that I believe we’re now at a point where the company offers good long-term value for conservative dividend growth investors looking to buy undervalued stocks.

Although I’m still in the camp that believes that inflation will remain a longer-term issue, buying high-quality, beaten-down stocks is a great way to build long-term wealth.

So, let’s get to the details!

Hormel Foods Is Improving

One of the reasons why HRL shares have performed so poorly since my prior article is its performance on October 12, 2023.

On that day, the Wall Street Journal reported that “Hormel Foods Stock Just Had Its Worst Day Since 2008.”

Shares of Hormel Foods fell after the food maker laid out a three-year plan that includes a handful of financial targets and reached a new deal with workers represented by the United Food and Commercial Workers International Union.

The stock slipped by nearly 10%, marking its biggest percentage decline since October 2008. The stock is down almost 29% this year, which would mean its worst year on record in data going back to 1972.

The company on Thursday held an investor day and posted an accompanying presentation Thursday morning that lays out some long-term financial targets. Hormel plans to grow operating income by more than $250 million by fiscal 2026, including 5% to 7% growth from the current business.

At the end of November, the company held its 4Q23 earnings call, which elaborated on its plans to turn its business around.

One key growth opportunity lies in the company’s commitment to evolving into a global branded food entity. This strategic shift involves the implementation of a go-forward operating model, reflecting a proactive approach to meet changing market dynamics.

For example, the integration of the Jennie-O Turkey brand is a pivotal component of this evolution, contributing to the company’s broader goal of becoming a more diversified and internationally competitive player in the food industry.

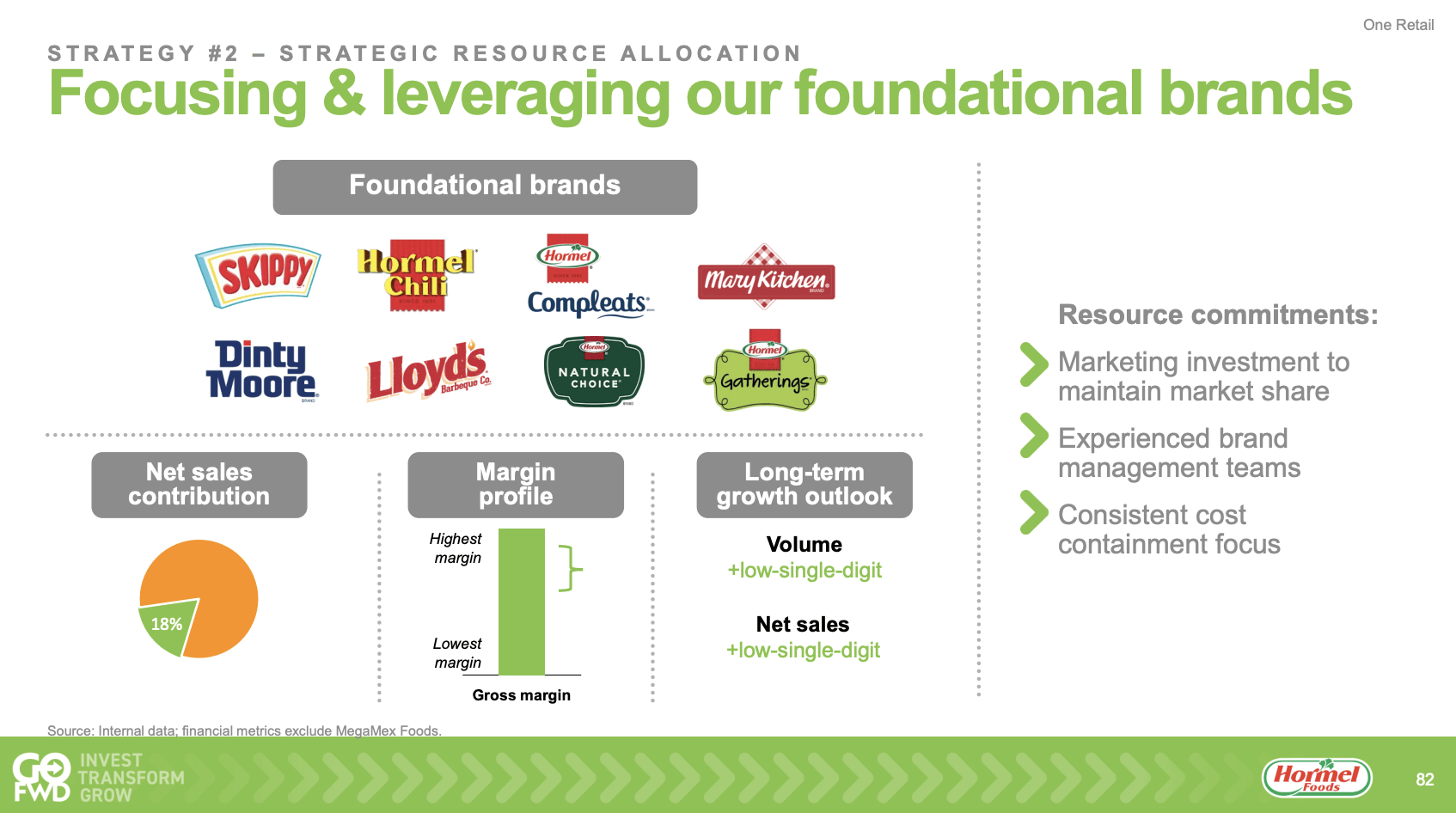

With a portfolio featuring brands such as Planters, Corn Nuts, Hormel Pepperoni, Columbus, and HORMEL GATHERINGS, the company is strategically positioned to capitalize on evolving consumer preferences.

In the retail segment, the company is strategically concentrating on driving focus and growth.

The implementation of a go-forward structure involving the combination of seven retail businesses and the establishment of a brand fuel center of excellence is designed to enhance strategic vision and operational efficiency.

Hormel Foods Corporation

This streamlined approach is expected to result in improved resource allocation, driving profitable growth and enhancing the overall margin structure of the retail business.

Hormel Foods Corporation

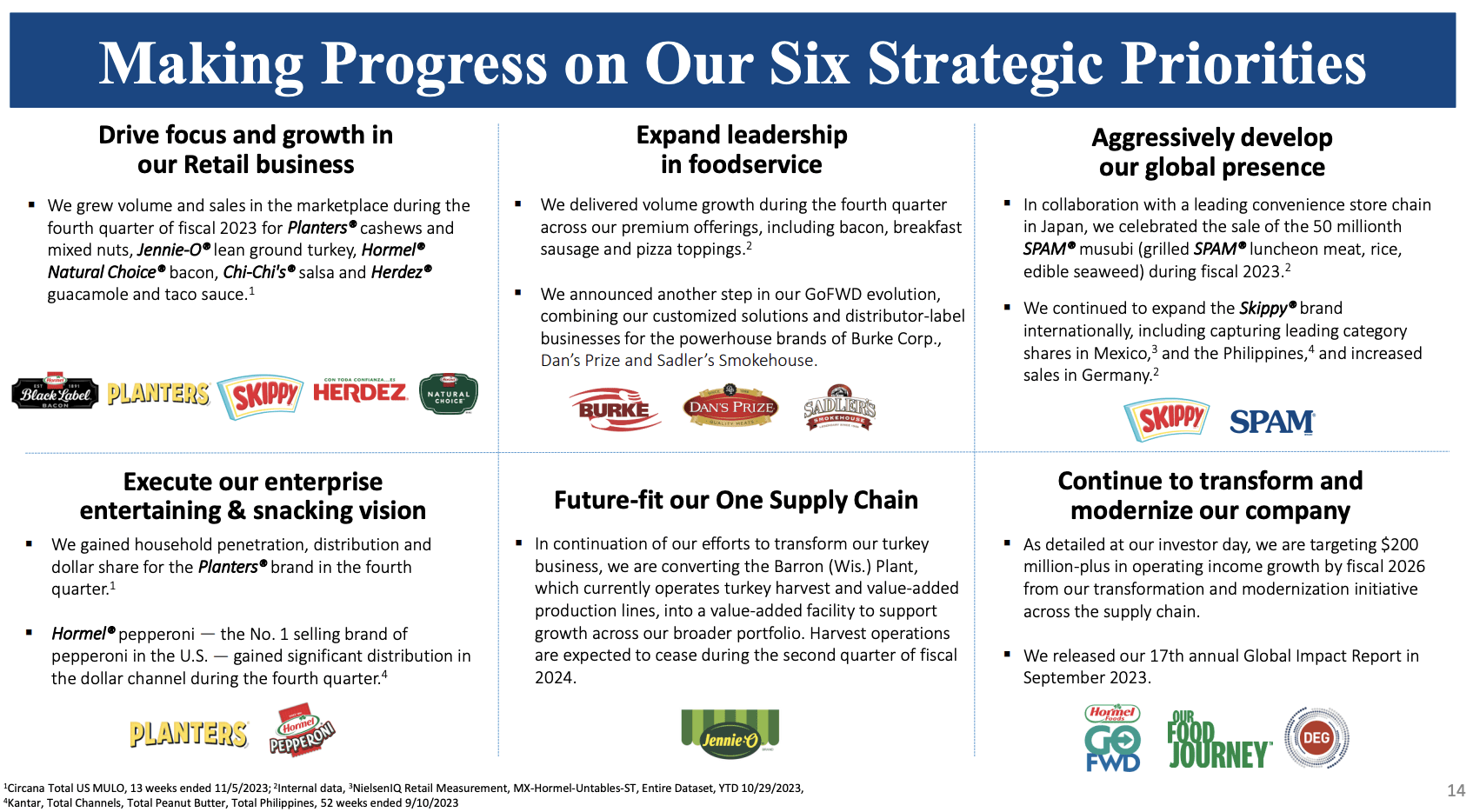

Furthermore, the company believes it is well-positioned to capitalize on growth opportunities in the food service sector.

Despite challenges faced during the pandemic, the food service business showed strength in fiscal 2023, and continued growth is anticipated in fiscal 2024.

Key categories such as bacon, pepperoni, prepared proteins, and turkey are areas where the company expects to accelerate growth.

Hormel Foods Corporation

Additionally, plans to establish a digital leadership position in the industry and expand presence in the convenience store channel reflect a forward-looking approach to industry trends.

Hormel Foods is also aiming for faster growth in markets like China.

According to the company, normalized shipments of key products to strategic markets and an easing of headwinds in commodity businesses are expected to contribute to the resumption of accelerated growth in the international segment.

For now, however, the overseas market is small, as the company generated just 5% of its sales outside of the United States in FY2023.

Furthermore, as part of the broader transition, the company is focusing on optimizing its supply chain.

For example, the conversion of the Barron, Wisconsin plant into a value-added facility is a major step toward reducing costs, minimizing complexity, and better aligning the turkey supply chain with changing consumer demands.

The actions at the Barron plant further right-size our turkey supply chain, supporting top-line growth, improved profitability and decreased exposure to commodity volatility. – WATTPoultry

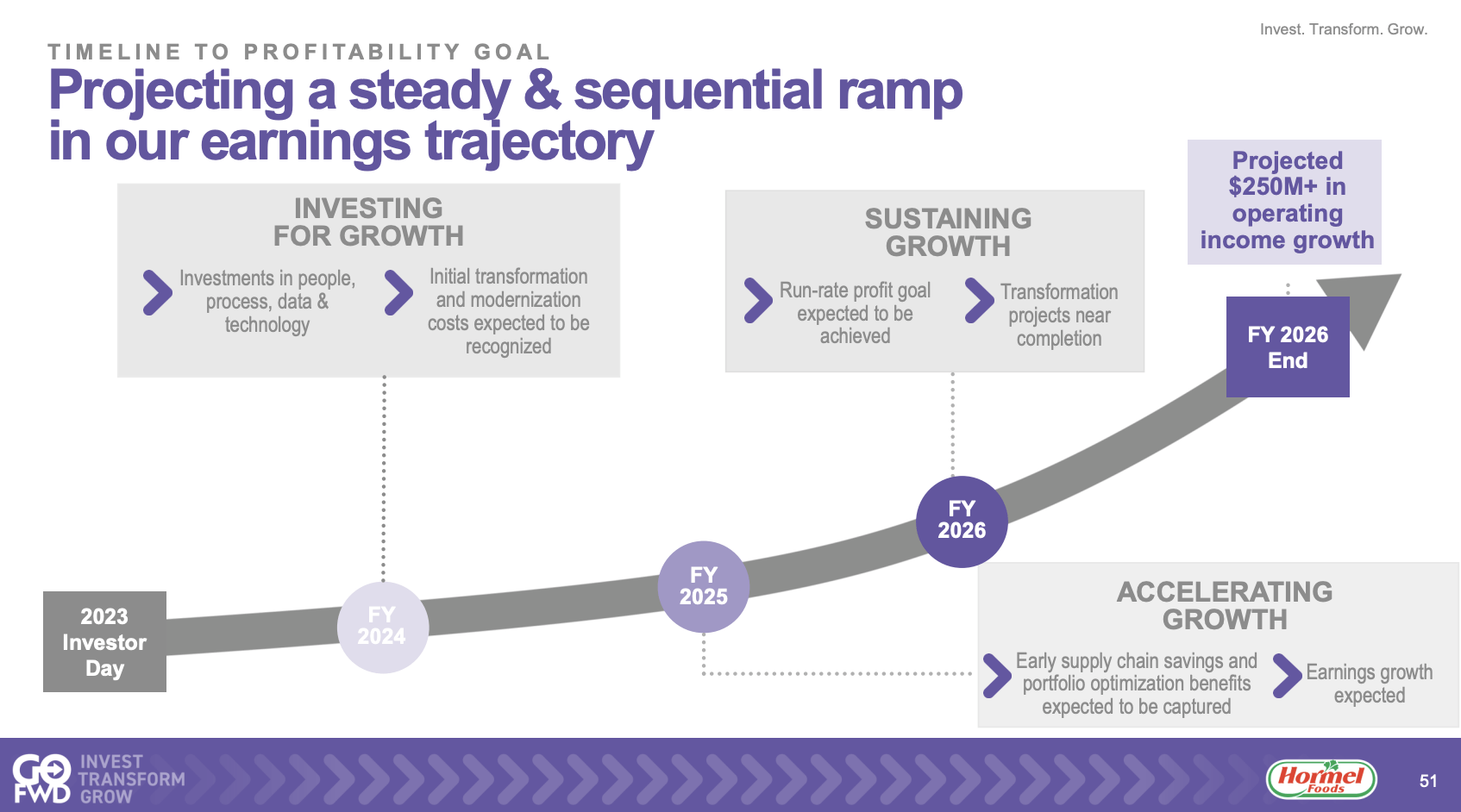

Based on everything said so far, the transformation and modernization initiative involve a significant investment of approximately $250 million over the next three years.

While fiscal 2024 is expected to see a modest benefit to net earnings, the initiative is projected to deliver substantial operating income growth of roughly $250 million by fiscal 2026.

Hormel Foods Corporation

With that said, let’s take a closer look at recent developments and shareholder value.

Where’s The Shareholder Value?

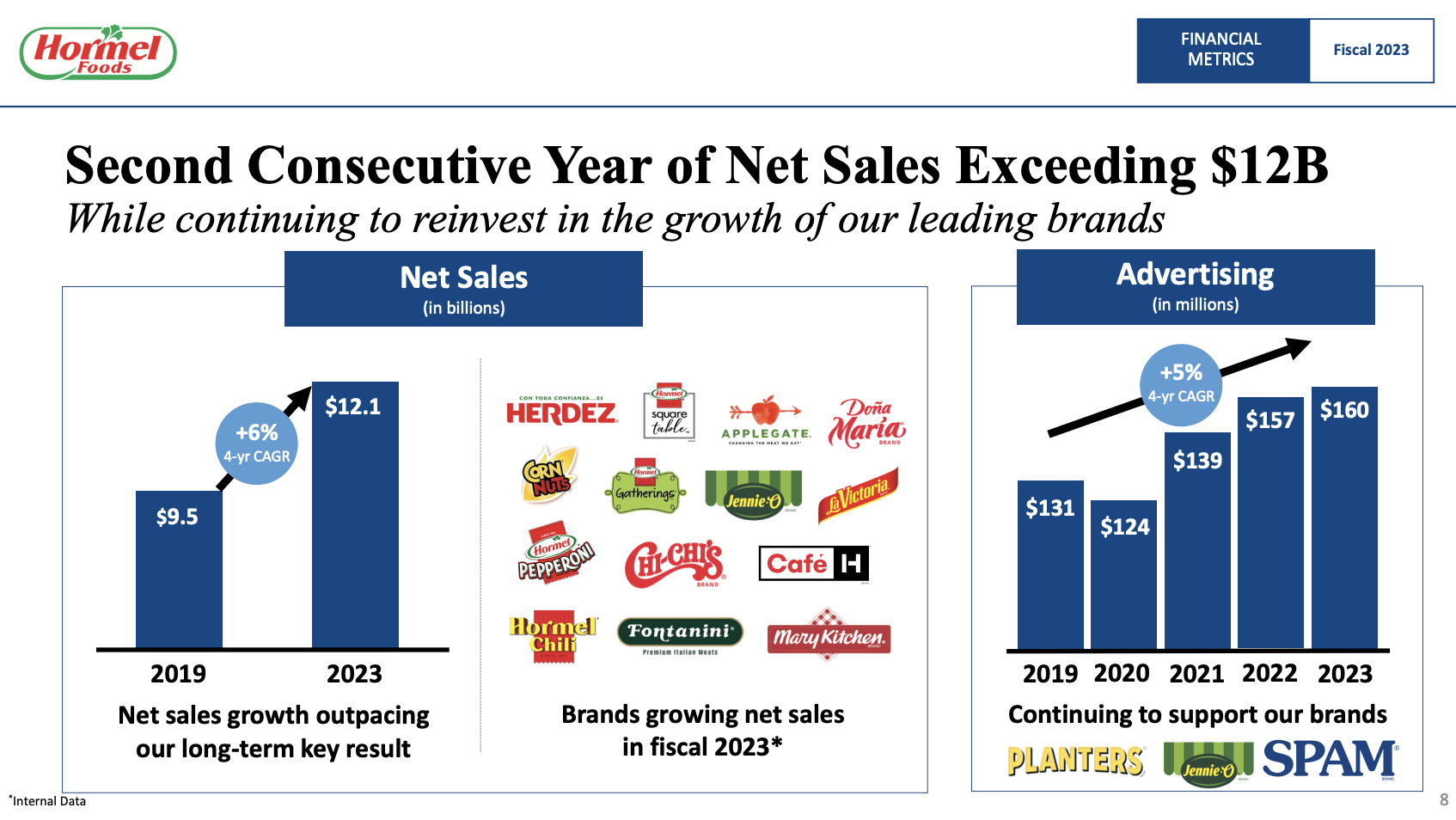

In the 2023 fiscal year, net sales reached $12.1 billion, marking the second-highest result in its history.

Hormel Foods Corporation

The company reported operating income of $1.1 billion (-9.8%) for fiscal 2023, with an adjusted operating income of $1.2 billion.

Operating margin and adjusted operating margins were reported at 8.9% and 9.8%, respectively.

Hormel Foods Corporation

Diluted net earnings per share for the full year were $1.45 (-11.4%). Excluding specific impacts, adjusted diluted net earnings per share stood at $1.61.

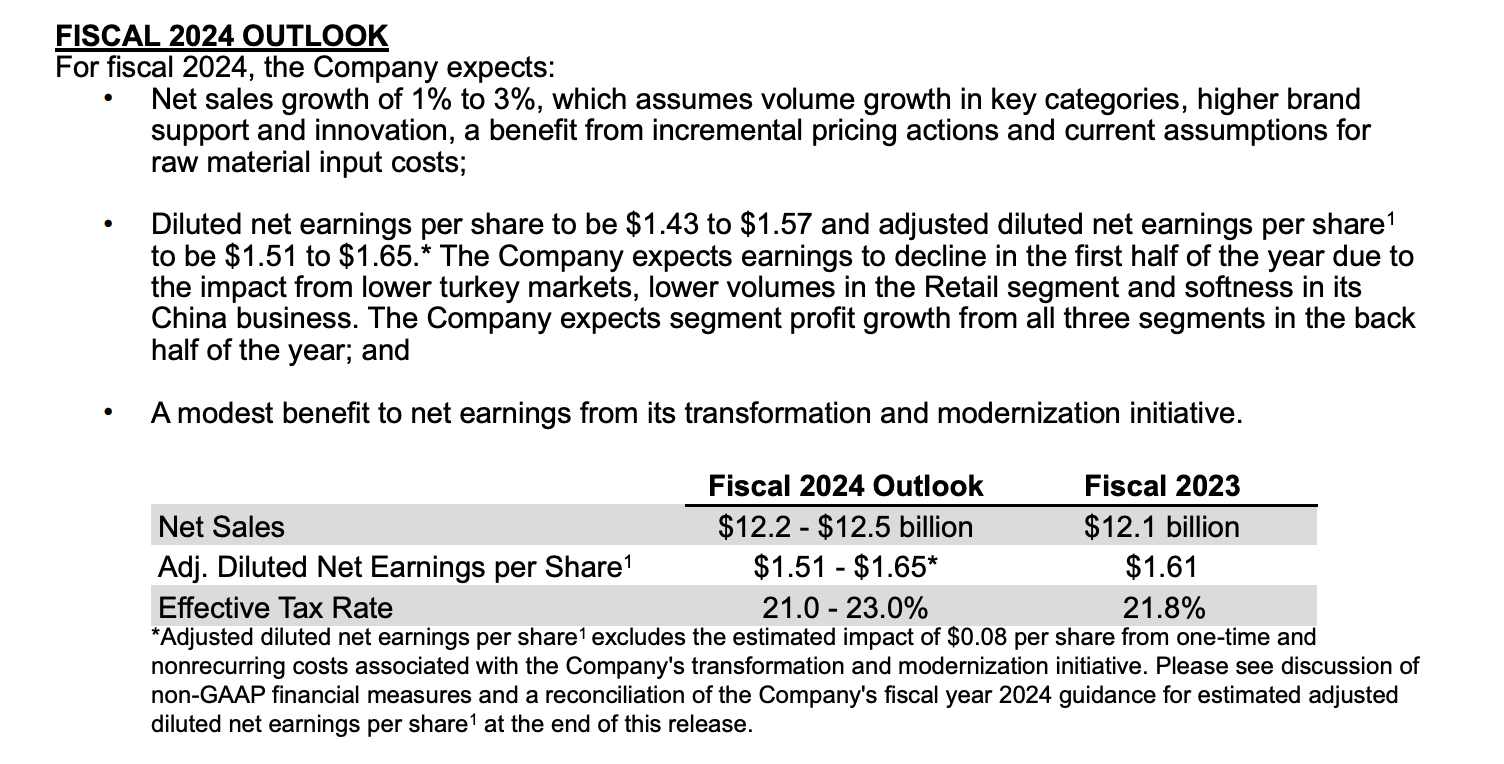

Looking forward to fiscal 2024, the company outlined its outlook and key investments during its earnings call.

It plans to invest in end-to-end planning capabilities, infrastructure, and software to enhance data and analytics capabilities.

Additionally, there will be a modernization of the order-to-cash system, with incremental headcount to support various work streams across the supply chain.

Approximately one-third of the total investment is expected to be recorded in fiscal 2024, with around $0.08 EPS classified as one-time and the rest either capitalized or included in the ongoing cost structure of the business.

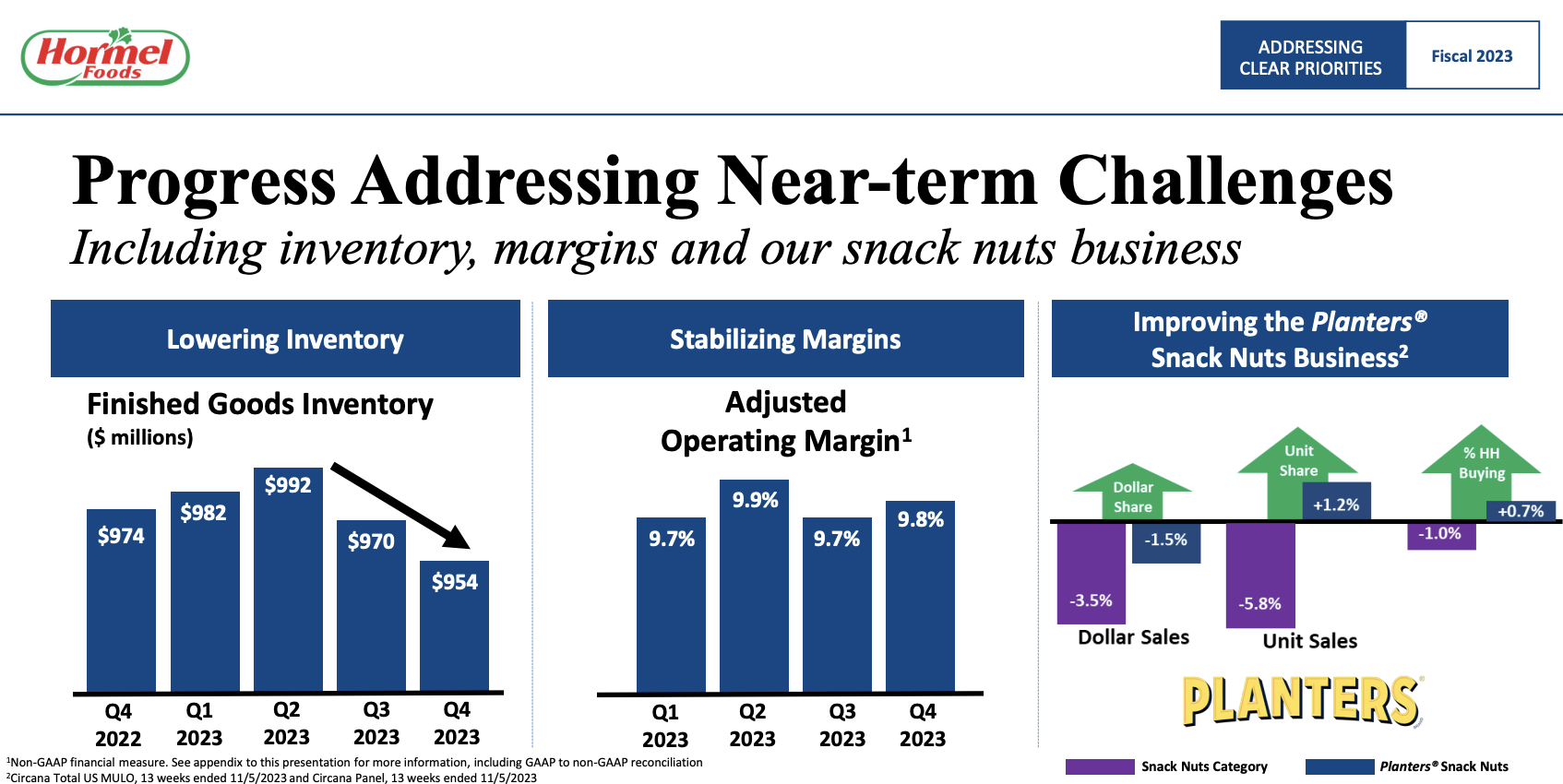

As we can see in the overview above, in terms of inventory management, the company successfully achieved its goal of reducing inventory, with inventories finishing the year at $1.7 billion, a decrease of $36 million from the beginning of the year.

This reduction shows effective supply chain management and responsible inventory levels to support targeted fill rates, which will support margins.

On a full-year basis, it expects to grow sales by $100 to $400 million, with uncertain adjusted EPS growth.

Hormel Foods Corporation

It also maintained a disciplined financial strategy.

The balance between debt and cash position was well-managed, with the company ending the year with $3.3 billion of debt and over $750 million in cash and short-term securities, aligning with its goal of 1.5 to 2x net debt to EBITDA.

The company has a credit rating of A-, which is one of the best ratings in its sector.

As a result, the company has a strong focus on its shareholders.

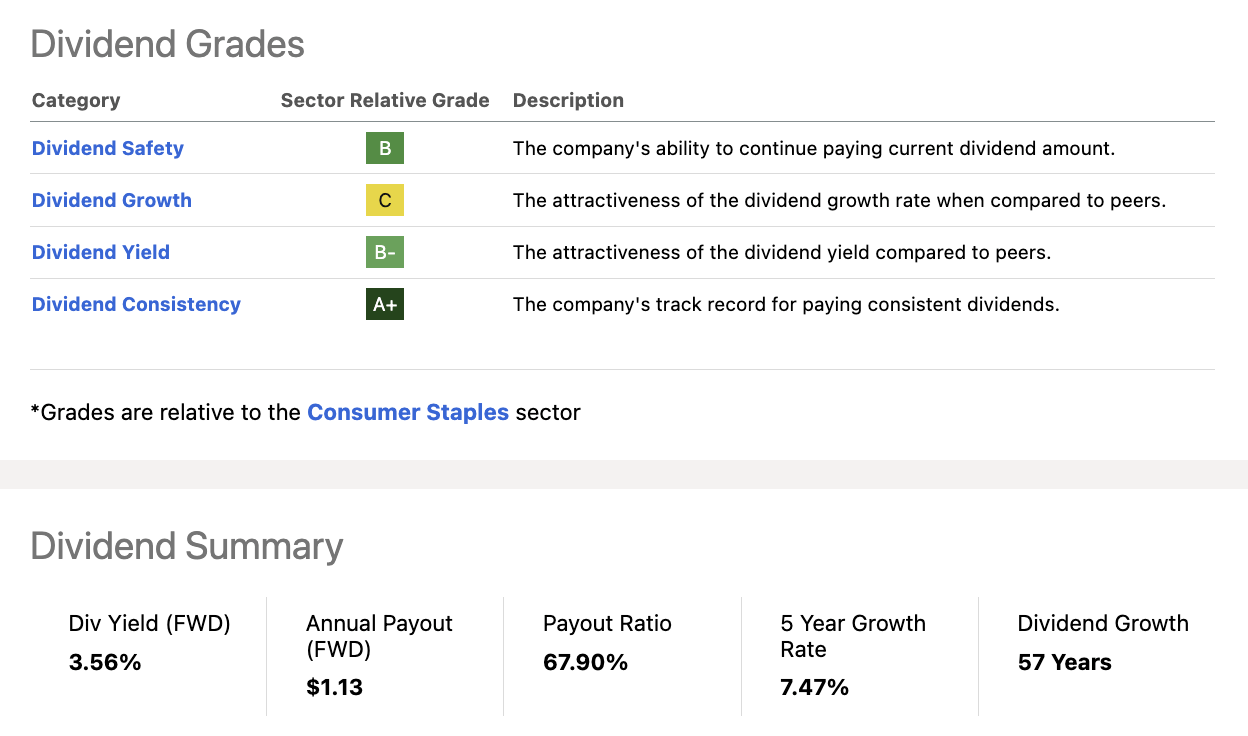

In the fourth quarter of the 2023 calendar year, the company announced a 3% increase in the annual dividend to $1.13 per share for fiscal 2024.

This marks the 58th consecutive year of dividend increases and translates to a yield of 3.6%. Eight years ago, the company became a dividend king with 50 consecutive annual dividend hikes.

The five-year dividend CAGR is 7.5%. Dividends are protected by a sub-70% payout ratio.

Seeking Alpha

If the company is able to turn its business around, I have little doubt that it can return to mid-single-digit annual dividend growth, which could add tremendous shareholder value.

Speaking of value, the stock is attractively valued.

Using the data in the chart below:

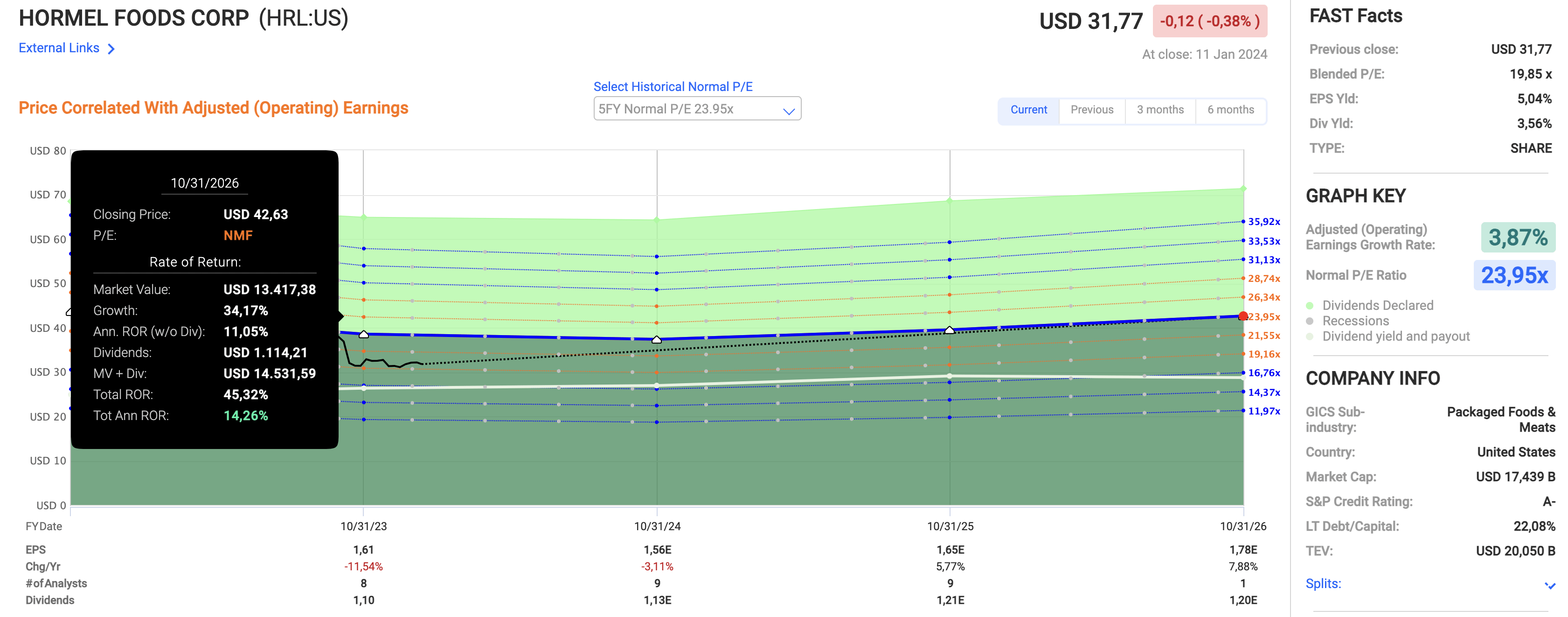

HRL is currently trading at a blended P/E ratio of 19.9x

The five-year normalized valuation is 24.0x, which is appropriate, given the company’s expected growth trajectory.

Although EPS is expected to decline by 3% in FY2024, in line with HRL guidance, analysts see 6% growth in 2025 and up to 8% growth in 2026.

While these numbers are subject to change, they indicate that an earnings bottom could be near. When adding the dividend and a potential return to a higher valuation, the stock could return 14% per year through 2026.

Since 2003, HRL has returned 9.7% per year, despite falling 40% since 2022!

FAST Graphs

Needless to say, I cannot guarantee a >14% return, especially because I believe that sticky inflation could keep a lid on its valuation.

However, given company measures to boost profitability and streamline overall operations on top of its attractive valuation, I believe that HRL makes for a good long-term investment at current prices.

Takeaway

Despite recent challenges and a significant drop in stock value, Hormel Foods is strategically positioning itself for a turnaround.

The company’s focus on global expansion, digital leadership, and operational efficiency, coupled with a commitment to shareholder value, presents an attractive investment opportunity.

While dealing with the impact of persistent inflation on valuation, HRL’s current stock price, blended P/E ratio of 19.9x, and potential for future growth indicate a favorable long-term investment.

Investors, especially those seeking conservative dividend growth, may find HRL’s current undervalued position a promising entry point for building wealth over the next few years.

Q2 2024 Earnings Call Transcript")