“A nickel ain’t worth a dime anymore.”

Social Security recipients might empathize with that Yogi Berra quote. Benefits payments began including the 3.2% cost-of-living adjustment (COLA) this month. However, a recent survey conducted by public interest law firm Atticus found that 62% of seniors aren’t happy with the amount of their Social Security increase.

But if you’re disappointed in your Social Security uptick for this year, it might help at least a little to gain some historical perspective. Here’s what the average COLA has been since 2000.

Image source: Getty Images.

2024’s Social Security COLA is higher than average

We can easily fall sway to recency bias. It’s the tendency to put more emphasis than is warranted on more recent events. As a case in point, some retirees could compare the 3.2% COLA announced in October 2023 to the 8.7% increase announced a year earlier. With that comparison, the latest boost seems paltry.

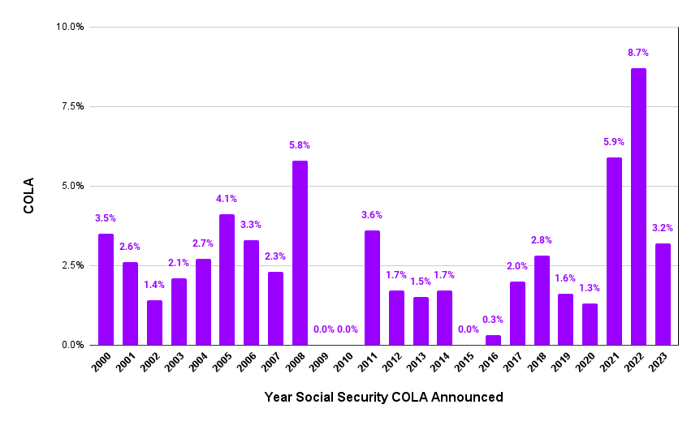

However, looking back further reveals a very different picture. The chart below shows the annual Social Security COLAs by the year they were announced beginning in 2000.

Data source: Social Security Administration. Chart by author.

Sure, the most recent Social Security COLA is well below the increase received in the previous two years. However, it’s higher than the COLAs issued in 16 of the 24 years displayed on the chart. Note that there was no boost in three of those years. The average COLA during this period was 2.6%, well below the uptick that went into effect this month.

Why next year’s increase could be even smaller

I suspect that knowing that your current COLA beats the average increase for the 21st century provides little comfort for most people. If you’re in that group, I have some bad news for you: Next year’s increase could be even smaller.

COLAs are based on inflation. And inflation appears to be moderating. The Federal Reserve raised interest rates aggressively in 2022 to try to bring inflation down. Those efforts seem to be paying off.

Many Americans are taking notice, too. The Federal Reserve Bank of New York’s December Survey of Consumer Expectations found that respondents’ attitudes about inflation have improved significantly. Consumers expect that the inflation rate will fall to 3% in 2024. The Fed thinks that its favorite inflation metric — the core personal consumption expenditures price index — will decline to 2.4% this year.

It’s important to note, though, that the Social Security Administration (SSA) calculates annual COLAs using a different inflation number called the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Also, the SSA only compares the third-quarter average CPI-W against the Q3 average from the previous year to determine the COLA.

We’ll therefore have to wait until October to find out what the next COLA will be. But for what it’s worth, the CPI-W has declined each month since September 2023. If this trend continues, your next COLA will almost certainly be lower than 3.2%.

A good reason to be disappointed about your Social Security COLA

Am I arguing that you shouldn’t be disappointed about your Social Security COLA? Not at all. Even though the increase is higher than the average over the last 24 years, there’s still a good reason to be unhappy about it.

The dissatisfaction with the latest Social Security boost shown in the Atticus survey indicates that many seniors feel that the COLA isn’t enough to cover the higher costs they’re incurring. And they have a point. The CPI-W metric that the SSA uses to calculate COLAs doesn’t reflect the costs that seniors incur as well as it could. In particular, healthcare expenses don’t receive a large enough weight.

Unfortunately, this will be a problem regardless of what the Social Security COLA is. There’s a potential fix (replacing the CPI-W with a metric that better reflects seniors’ costs). Perhaps this change will be implemented in the not-too-distant future. But that reminds me of another Yogi Berra quote: “The future ain’t what it used to be.”

Q2 2024 Earnings Call Transcript")