kadmy/iStock via Getty Images

I last wrote at Seeking Alpha about one of the most popular cannabis stocks in the world, Canopy Growth (NASDAQ:CGC) almost a year ago in late January, calling it not a good stock for cannabis investors. The stock has declined 82.6% since then, and this is a lot more than the market. The New Cannabis Ventures Global Cannabis Stock Index has dropped 19.6% since then.

When I reviewed the company, I pointed out that the company was executing a plan to keep its NASDAQ listing while transforming its business to an American cannabis operator through closing certain acquisitions that weren’t likely to help the stock. I suggested that if it failed to do so, then investors would be stuck with a poorly performing company with a high valuation. This hasn’t yet been resolved, but the stock has fallen a lot more than the 48% decline I predicted.

Last week, the stock dropped 4.8% and is down 11.5% in 2024. The Global Cannabis Stock Index is up 4.9% so far. The reason for the decline was an equity offering that was announced on Tuesday morning, with the company selling 7 million shares at $4.29 to institutional investors in a private placement. On Friday, very late in the day after the close, Canopy Growth revealed that the deal has been cancelled, at least for now.

SEC Filing

In this quick review, I discuss why investors should continue to avoid the stock.

The Fundamentals

Canopy Growth continues to have financial challenges. In that 8-K above, it stated that it expects to report its Q3 ending 12/31 on February 9th. According to Sentieo, analysts project that revenue will drop nearly 25% from a year ago to $75 million. Adjusted EBITDA is expected to be -$14 million.

The outlook remains pretty dim, as analysts expect FY24 revenue to decline 18% to C$329 million with adjusted EBITDA of -C$101 million. For FY25, they project revenue will rise 2% to C$336 million with adjusted EBITDA of -C$16 million. In the article a year ago, the FY25 outlook was for revenue of C$619 million with adjusted EBITDA of -C$84 million, so things are moving towards lower revenue and smaller losses.

As bad as its operations have been, this is not the biggest problem. The company’s balance sheet remains a huge challenge. After its Q2, the company reported tangible book value of C$517 million. Cash was C$270 million, but debt was C$681 million. The company used C$227 million to fund its operations in H1.

Canopy Growth has been trying to keep its NASDAQ listing while closing on the acquisitions of Acreage Holdings (OTCQX:ACRHF), Wana Brands, and Jetty, but it hasn’t yet made progress with the exchange. As I said a year ago, this will not save the company, as American cannabis operators will pursue an uplisting strategy if it is possible.

The Valuation

The share count has gone up a lot. The company reverse-split 10 shares for 1 recently. At the time they filed the 10-Q for Q2, they had effectively 83 million shares. Adding in the RSUs and PSUs, the total was 84.5 million. This was up from 72 million three months earlier. At C$6.01, the market cap is C$507 million, which is about tangible book value. A year ago, it was trading at 1.3X. Note that the three Canadian LPs that I include in my model portfolio all have better balance sheets and trade at a discount to tangible book value.

The enterprise value works out to be C$918 million, or 2.7X projected revenue for FY25 ending March 31. This is not appealing at all! My favorite cannabis stock, Organigram (OGI), which trades at just 0.7X tangible book value, has a market cap of C$189 million and an enterprise value of C$155 million. It trades at just 0.8X projected FY25 revenue. Unlike Canopy Growth, Organigram has positive projected adjusted EBITDA.

Despite the plunging price, I see the stock as a sell still. Constellation Brands (STZ) is deeply underwater in its investment and could step in and buy them, but the current situation with the company trying to keep its listing while closing U.S. acquisitions gets in the way. I think the stock should trade at 50% of tangible book value given its large debt, continued operating losses, and use of cash flow. If it were to trade there now, that would be C$3.06, which would be US$2.28, down another 50%.

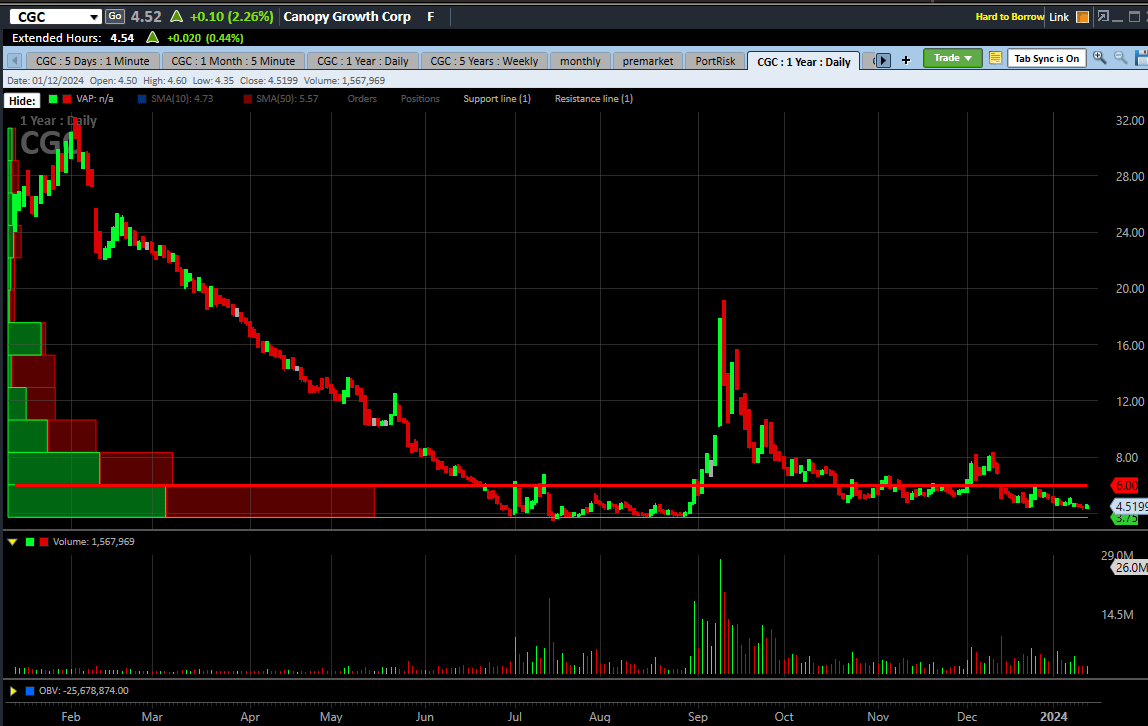

The Chart

Canopy Growth put in an all-time low of $3.46 in mid-July when it closed at a record-low $3.74, and this could get tested in my view:

Charles Schwab

The run-up in September was an error by investors who got excited about the U.S. potentially rescheduling. I see $3.75 as potential support on the chart and $6.00 as resistance.

Conclusion

I generally like to buy the dips, but I am not at all interested in adding Canopy Growth to my Beat the Global Cannabis Stock Index model portfolio. I think the stock should be trading 50% lower. It has a lot of debt and negative operating cash flow.

The equity sale, which is necessary to fix their financial condition and which is likely to happen in the near future, was cancelled. Perhaps the stock will bounce on this news, giving shareholders a chance to exit at a higher price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")