Yok_Piyapong/iStock via Getty Images

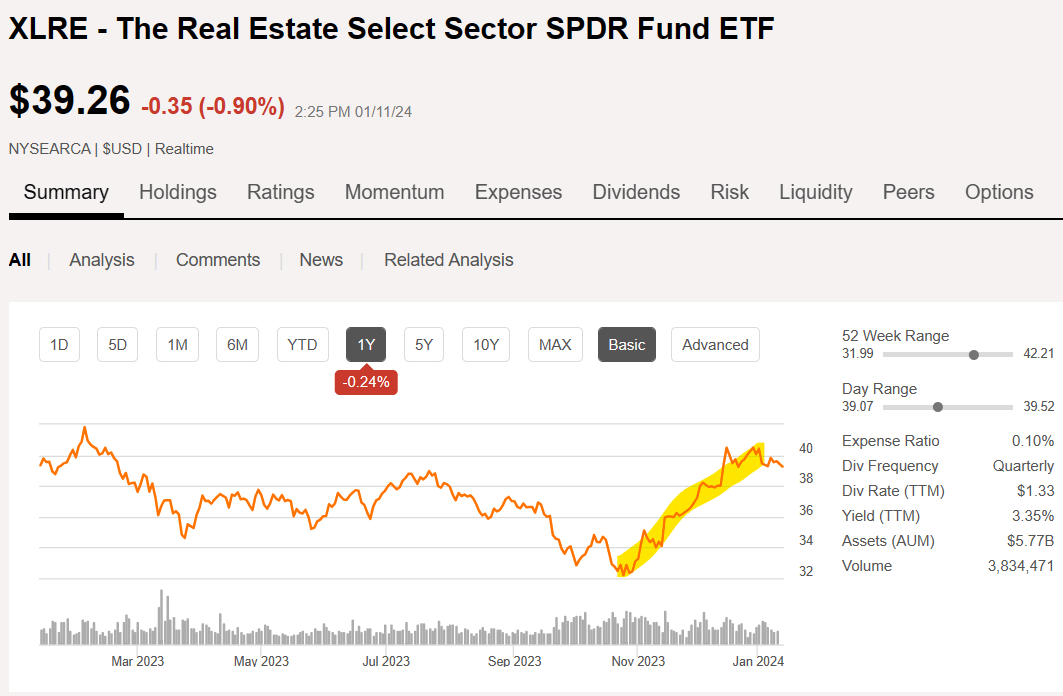

While retirees and those saving for retirement seek to increase their passive income from investments, one asset class that offers a high yield income to support that goal is real estate. Historically, REITs (real estate investment trusts) have delivered outstanding returns due to their favorable tax structure and offer diversification from traditional equities. However, they also tend to be very sensitive to interest rate risk. As a result, the real estate sector was one of the worst performing market sectors in 2023 due to rapidly rising interest rates. But that trend changed back in November, when the Federal Reserve began to hint at the potential for reducing rates in 2024. This shift can be seen in the chart for XLRE.

Seeking Alpha

Now in the second week of the new year, real estate has become the top performing market sector after hitting that low point at the end of October. One company that operates as a REIT and stands to benefit from a reduction in interest rates this year is Ellington Financial (NYSE:EFC). Ellington is a unique REIT that seeks to generate attractive, risk-adjusted returns using an opportunistic strategy across various types of mortgage-related, consumer, and corporate loans and securities. The company was founded in 2007 and is based in Old Greenwich, CT. From the company website:

Ellington Financial invests in a diverse array of financial assets, including residential and commercial mortgage loans, residential and commercial mortgage-backed securities, consumer loans and asset-backed securities backed by consumer loans, collateralized loan obligations, non-mortgage and mortgage-related derivatives, strategic debt and equity investments in loan origination companies, and other strategic investments.

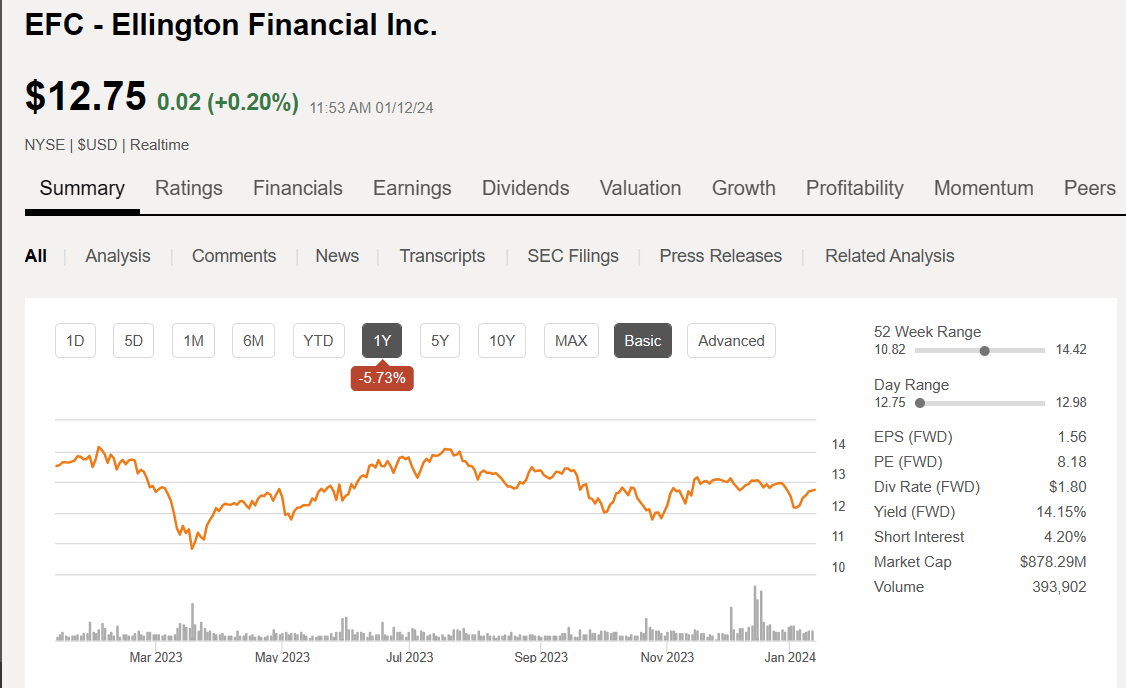

From an income investors’ perspective, EFC offers a generous monthly dividend of $0.15 which equates to an annual yield of 14% at the current market price of $12.75. I rate EFC a Buy given the company’s strong financial position, the recent acquisition strategy and prospects for continued growth and recovery in the real estate market. The most recent estimate of book value in December 2023 was $14.06 as of November 30, so the stock is trading at a discount of about -10% before considering the additional book value to be realized as a result of the merger with Arlington Asset Investment Corp, which was completed on December 14, 2023.

The AAIC acquisition should lead to a larger market cap, additional low-coupon MSRs, and attractive long-term unsecured debt to help strengthen the balance sheet. The acquisition is expected to drive earnings accretion beginning in 2024.

Hybrid REIT Model

Although EFC tends to be lumped in with other mREITs their business model is more of a hybrid REIT, allowing them to strategically pursue opportunities in various asset classes. The target asset classes that the company focuses on includes agency RMBS, CLOs, CMBS and commercial loans, consumer loans and ABS, mortgage-related derivatives, non-agency RMBS, residential mortgage loans, and strategic debt and equity investments in loan originators.

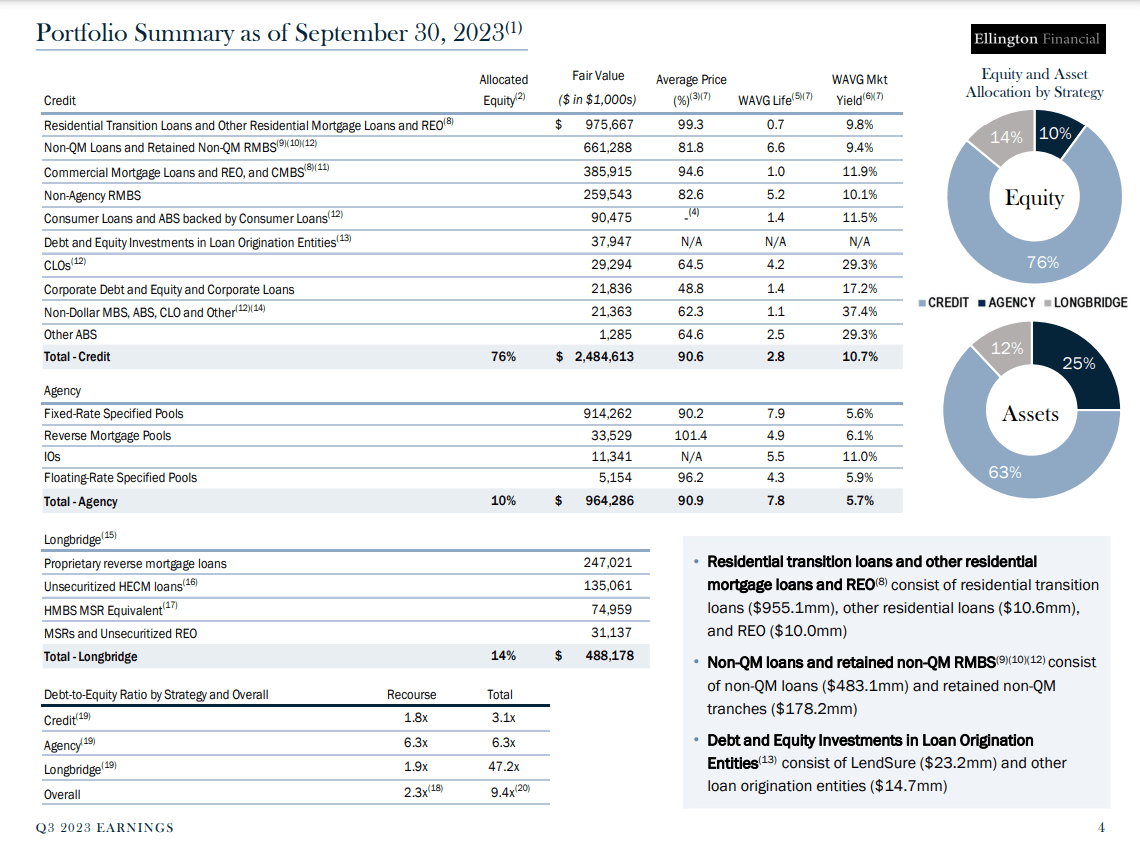

Approximately 76% of the total portfolio is invested in credit related equity, while 10% is invested in agency equity, and 14% in Longbridge Financial equity. Longbridge was acquired by EFC in October 2022 and specializes in reverse mortgages and HECM loans. This slide from the company’s Q323 earnings presentation shows the breakdown by equity and asset type as of 9/30/23.

Ellington Financial

The long credit portion of the portfolio increased from $2.45 billion in Q2 to $2.48 billion in Q3. The increases were mostly due to larger non-QM and residential loans as net purchases exceeded loan paydowns, and an increase in non-agency RMBS which also saw net purchases increase. The long agency portfolio also increased by 5% from $918.5 million in Q2 to $964.3 million in Q3 as opportunistic purchases exceeded sales, principal repayments, and net losses. In Q3, the Longbridge portfolio increased by 14% from $429.8 million to $488.2 million. Most of that increase was due to proprietary reverse mortgage originations and the acquisition of an MSR portfolio from a bankruptcy proceeding on July 1.

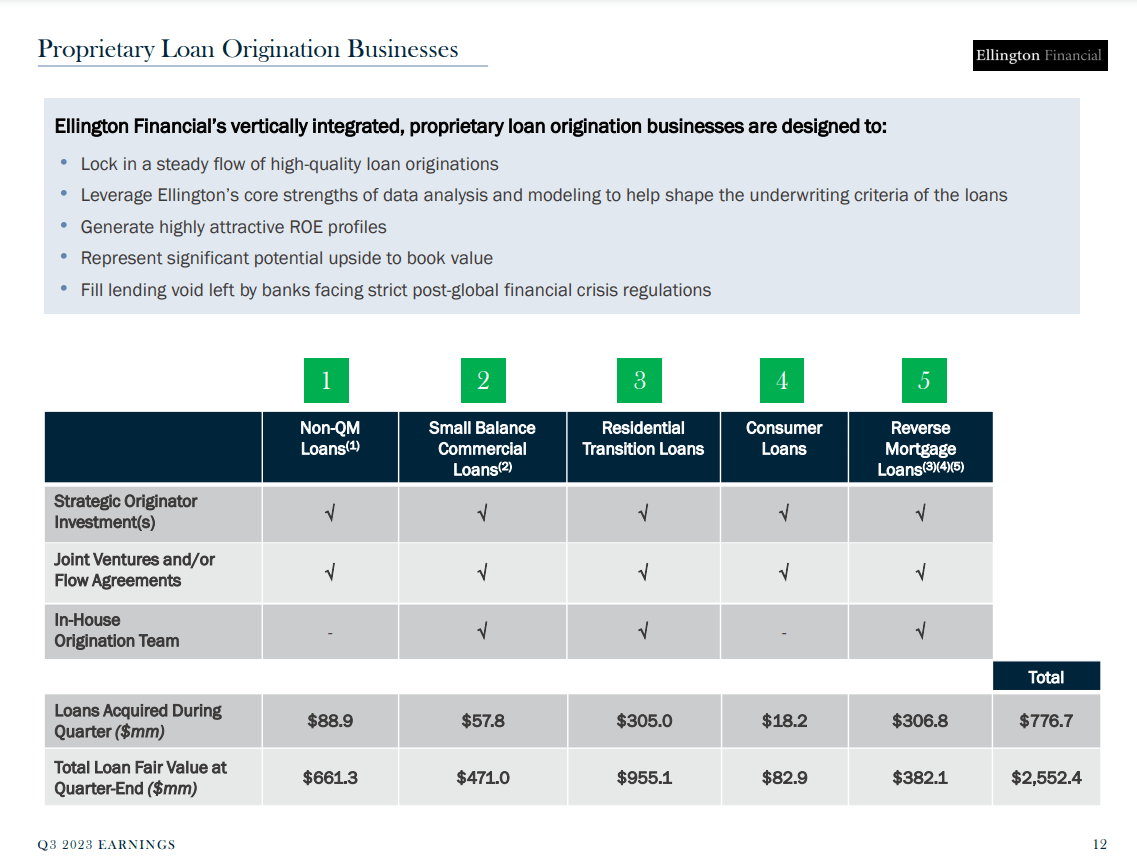

The small balance commercial mortgage loan portfolio consists of 100% senior first lien, floating rate loans, diversified across geographies and property types with about two thirds multi-family. Roughly $58 million in new commercial loans were acquired in Q3. Commercial loans make up roughly 20% of the overall credit portfolio, while residential mortgages of various types (non-QM, residential transition, NPL/RPL, non-agency, REO, and single-family rental MBS) make up the majority at 74%. Consumer loans account for about 4% and other diversified financial instruments account for the remaining 2%.

The Ellington proprietary loan origination business is vertically integrated and high performing. The majority of new loans originated during Q3 were reverse mortgage and HECM loans via the Longbridge subsidiary, which represents significant upside potential, although still a relatively small percentage of the overall loan portfolio.

Ellington Financial

Book Value Supported by Interest Rate Hedge

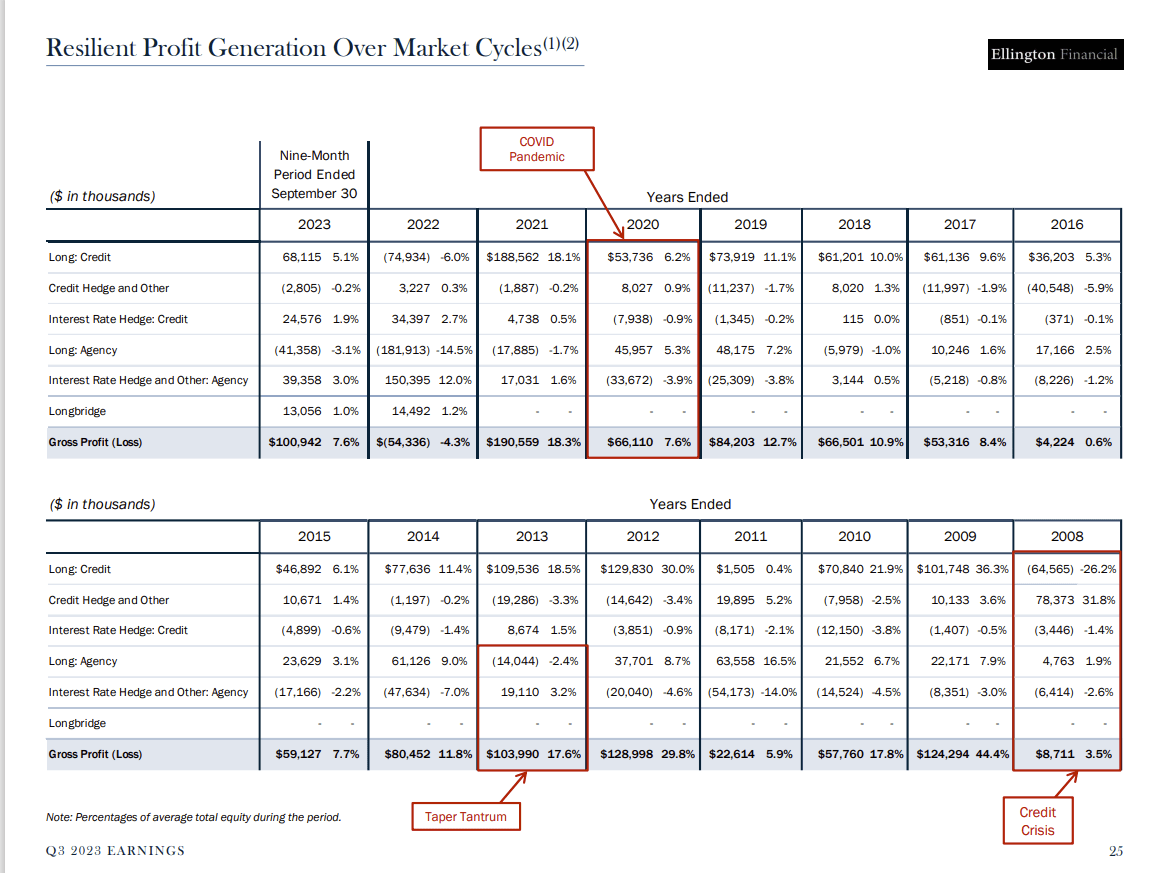

Ellington uses a sophisticated, dynamic approach to interest rate hedges. That strategy has helped to preserve book value and generate profits even during difficult times including the GFC, Covid pandemic, and other difficult periods during the past 15 years. In fact, 2022 was the first year since the company was founded that they reported a loss on the year, as shown on this slide from the Q3 presentation.

Ellington Financial

As explained by CEO Larry Penn on the Q3 earnings call, the hedging strategy has worked well for EFC ever since they went public in 2007:

Going back to the launch of EFC in 2007, we’ve never tried to predict the direction of interest rates and have instead endeavored to hedge them. In this past quarter with interest rates spiking, our interest rate hedges were again very profitable and that helped offset mark to market losses on other parts of the portfolio. The extreme pace of rate hikes since last year clearly caught a lot of the market off guard, but our hedging has kept EFC relatively unscathed.

Picking up the Slack

Looking to the future, the MSR portfolio acquired by Longbridge in July is already returning strong results and should contribute to future earnings growth, along with the newly acquired agency MSRs from Arlington. As discussed by CEO Penn on the Q3 earnings call, the opportunities to expand the agency MSR portfolio with the Arlington acquisition are likely to result in strong returns as banks are starting to lean away from the mortgage lending business.

The ongoing dislocation of the banking sector should continue to generate compelling opportunities for Arlington Financial, both to buy distressed assets and to add market share at our originator affiliates. Banks are under pressure from regulators and from losses on their loans and securities. And with deposits leaving for higher yielding alternatives, we see an inefficient market getting even less efficient. Banks stepping back means less capital available to make or buy loans, which should put upward pressure on the spreads we can earn. The opportunities in distress commercial mortgage loans and CMBS could be particularly compelling.

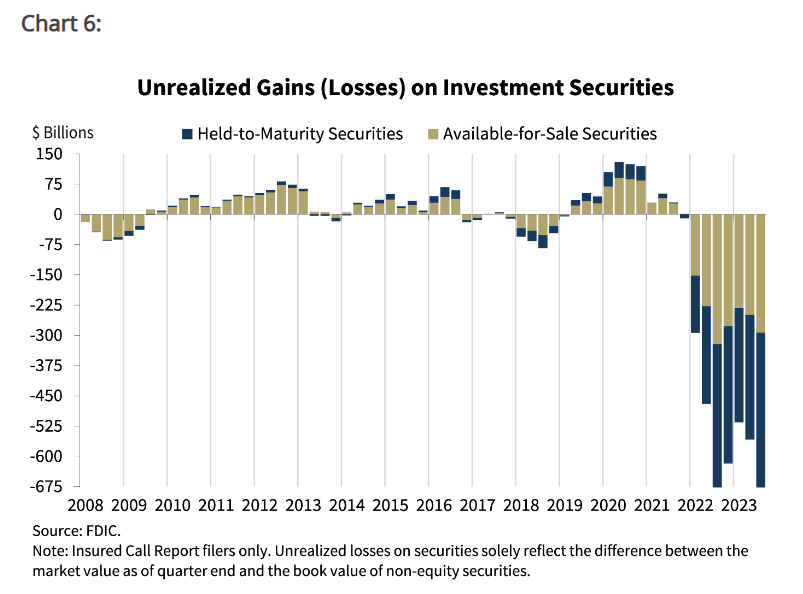

For example, the FDIC has already begun putting up for sale the failed Signature Bank commercial loan portfolio, with 20% of it sold to a Blackstone controlled entity in December. More banks are divesting their real estate loan portfolios and the trend is likely to continue, as discussed by the FDIC in this quarterly banking update.

On an annual basis, the banking industry continued to report a moderation in lending. The annual loan growth rate declined to 2.9 percent in the third quarter, reflecting surveys that indicate lower loan demand and tighter underwriting standards compared to last year.

The next chart shows that the banking industry’s holdings of longer–term loans and securities declined for a third consecutive quarter. The ratio of longer–term assets to total assets is 37.5 percent, still above the pre–pandemic average of 35.0 percent. The quarterly decline was led by a reduction in securities portfolios. Loans and securities with fixed, lower yields may pressure earnings in coming quarters.

FDIC

This dislocation in bank lending provides an opportunity for Ellington to pick up the slack and buy distressed loans at fire sale prices. When asked about the pending sale of the Signature Bank CRE portfolio on the Q3 earnings call, Co-Chief Investment Officer Mark Tecotzky had this to say:

So I think there is a big signature portfolio that’s been well publicized. But there is going to be just constant flow of properties where the debt is hitting a maturity date and they might require some sort of capital infusion or some sort of restructuring. And that’s — I think, we spoke about on the previous call, that was really the bread and butter of our commercial loan strategy for years after the financial crisis. And so that team that drove really exceptional results in that strategy, that workout strategy for us, I’d say, that’s what we were doing primarily prior to 2017. That team is still in place, they’ve pivoted to bridge and they’ve added additional resources in terms of sourcing and workout capabilities, but that team has so much experience in doing these workouts. So we are really, really well positioned and excited about that being the future driver of returns for EFC 2024 and beyond.

Analyzing Risk: Debt Levels and Borrowing Summary

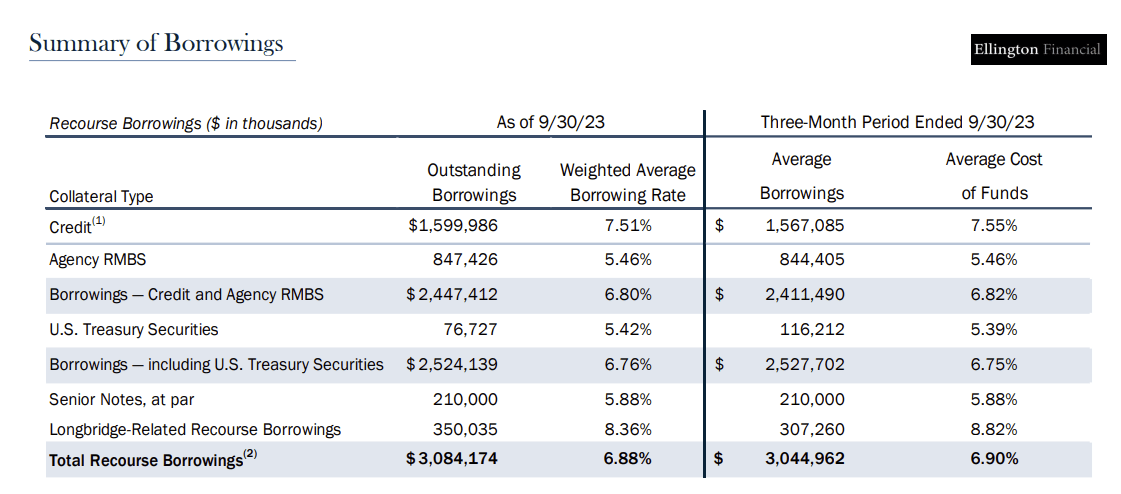

As explained by CFO JR Herlihy on the earnings call, net borrowings and debt to equity ratios increased slightly from Q2 to Q3, with the largest discrepancy in agency margins:

On our recourse borrowings, the weighted average borrowing rate increased by 21 basis points to 6.88% as of September 30th, driven by the increase in short term interest rates. Meanwhile, book asset yields on our credit strategy also increased over the same period and we continued to benefit from positive carry on our interest rate swap hedges where we net receive a higher floating rate and pay a lower fixed rate. As a result, the net interest margin on our credit portfolio expanded sequentially. However, an increase in the cost of funds on our agency strategy exceeded an increase in its book asset yields, which caused net interest margin on agency to decrease quarter-over-quarter.

Ellington

The debt-to-equity ratios also increased slightly, and book value declined from the previous quarter, but cash levels remained unchanged.

Our recourse debt-to-equity ratio adjusted for unsettled purchases and sales increased to 2.3:1 as of September 30th as compared to 2.1:1 as of June 30th. Our overall debt-to-equity ratio adjusted for unsettled purchases and sales also increased during the quarter to 9.4:1 as of September 30th as compared to 9.2:1 as of June 30th. At September 30th, our combined cash and unencumbered assets totaled approximately $569 million, roughly unchanged from the prior quarter and our book value per common share was $14.33, down from $14.70 in the prior quarter.

That debt-to-equity ratio of 9.4x (as of 9/30/23) is relatively high for an REIT, but is down from the high of 10.37x that it reached in December 2022. I suspect that part of the increase in the debt ratios is due to the Arlington acquisition and as those assets get rolled into EFC the ratio will come back down again. That is a risk to consider though if the economy does shift suddenly and the expected increase in the MSR business does not pan out the way that management expects.

Summary

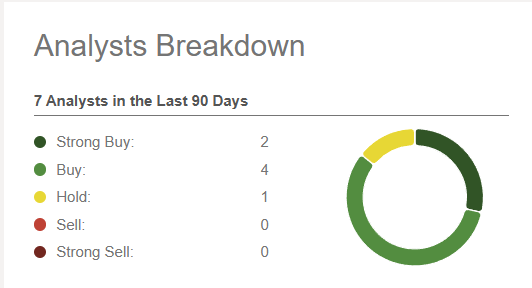

While Wall Street analysts are generally positive on EFC with 2 Strong Buy, 4 Buy, and 1 Hold rating, the average price target is $14.57, representing about 14% upside.

Seeking Alpha

The stock trades at about 90% of book value, offers investors a monthly dividend of $0.15 which represents an annual yield of about 14%, and is well positioned going forward to increase revenues and earnings from the additional MSR opportunities afforded by the Arlington acquisition.

Seeking Alpha

I feel that EFC offers income investors a unique buying opportunity while the stock trades at a price below $13, and I recommend buying shares while the price remains down due to ongoing fears of high interest rates. Once rates do start to come down (presumably later this year), I believe that the price of EFC will rise quickly as the real estate market recovers in 2024 and EFC reports improved earnings over the coming quarters.

Q2 2024 Earnings Call Transcript")