alexey_ds

Intuitive Surgical (NASDAQ:ISRG) announced its primary Q4 FY23 results on January 10th, preceding its presentation at the Annual J.P. Morgan Healthcare Conference. The stock price surged by 10.25% due to the strong results and outlook. I appreciate Intuitive Surgical’s leadership position in robotic-assisted, minimally invasive surgery. However, I believe their stock is overvalued by 45%. Consequently, I am initiating a ‘Sell’ rating with a fair value of $200 and encouraging investors to capitalize on the current gains.

Pre-Announced Earnings and FY24 Outlook

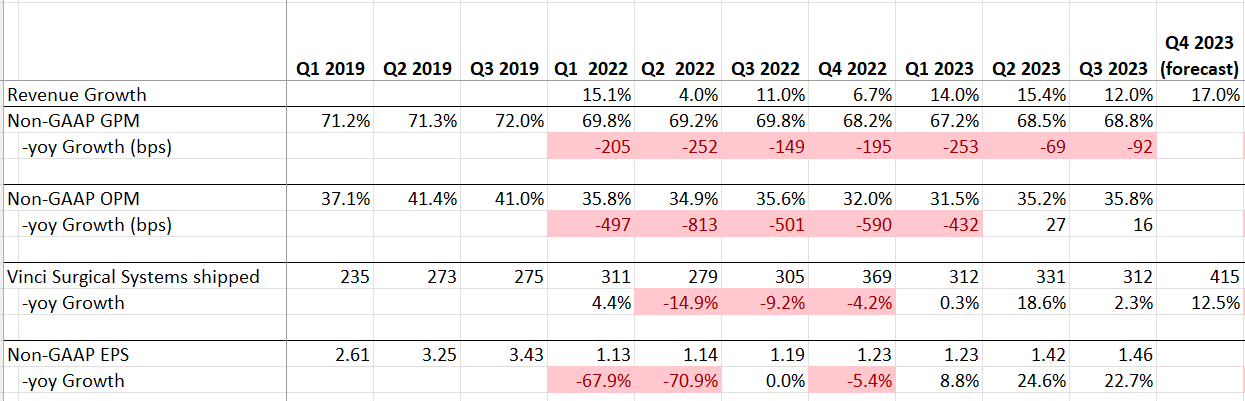

In Q4 FY23, da Vinci procedures experienced a robust growth of approximately 21%, and Intuitive Surgical placed 415 da Vinci surgical systems, indicating a notable 12% year-over-year growth. The company anticipates a substantial revenue increase of around 17% in Q4. These figures reflect impressive and robust growth for the company.

Intuitive Surgical Quarterly Earnings

The company anticipates a 13% to 16% increase in worldwide da Vinci procedures in 2024 compared to 2023, and this positive outlook significantly impressed the market, leading to a 10.25% rise in their stock price after the pre-announcement. I believe they are well-positioned for another year of robust growth in FY24 for several reasons.

Firstly, in Q4 FY23, they observed strong greenfield placements in the U.S. market, a robust indicator of hospitals making substantial capital investments. Given that surgeries tend to contribute more to hospital profits, the increased focus on surgical-related capital spending is encouraging. Moreover, robot-assisted surgery’s capability to perform minimally invasive operations could attract more patients to hospitals.

Secondly, the company achieved a remarkable 22% growth in procedures in FY23, and they attribute this to an elevated level of patients or backlogs in the healthcare system delayed by the pandemic. These backlogs are expected to continue driving procedure growth in 2024.

Lastly, their innovative products currently face no competition, and the projected 13% to 16% procedure growth aligns with historical trends. Historically, the company has delivered double-digit revenue growth with mid-teen operating income growth on average. According to the pre-announcement, their revenue is projected to grow around 14.5% in FY23, and I anticipate they should maintain around 14% growth in FY24, consistent with their historical trend.

It is important to note two potential factors that could impact their growth: the Chinese market and bariatric surgery, which I will discuss further later.

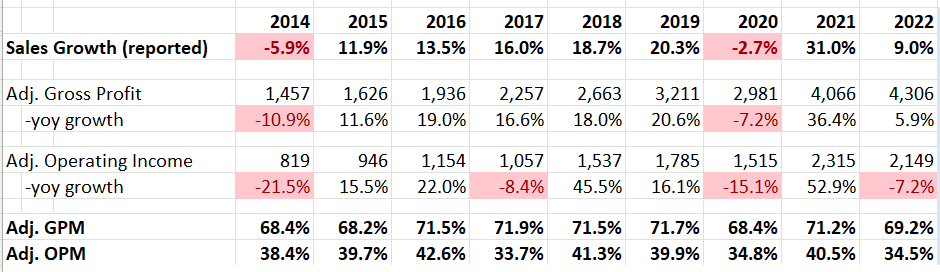

Intuitive Surgical 10Ks

Uncertainties in China

Since 2018, the China National Health Commission has determined the annual quota for major medical equipment sales in China. Furthermore, in 2022, the Hunan Provincial Healthcare Security Administration in China imposed significant restrictions on the fees hospitals can charge for surgeries utilizing robotic surgical technology, encompassing soft tissue surgery and orthopedics. Given the likelihood that other provinces may adopt similar measures, it poses a considerable challenge for Intuitive Surgical.

China stands as the second-largest market for procedures using Intuitive Surgical’s da Vinci system. The recent actions taken by Chinese authorities, combined with the government’s healthcare anti-corruption campaign, have led to delays in equipment purchases and surgical operations. The company faces considerable uncertainty in its Chinese operations, with factors such as pricing, tender quotas, and the duration of the anti-corruption campaign adding to the complexity. The lack of visibility into these variables may significantly impact the company’s overall growth rate.

Bariatrics Surgery

With the increasing popularity of GLP-1 drugs, there is a likelihood of a structured decline in demand for bariatric surgeries. During the JPM conference, it was acknowledged that there will be a continued deceleration of bariatric surgeries in the near term. I believe this trend will persist, creating headwinds for the company’s growth. GLP-1 drugs have proven to be quite effective for treating obesity patients.

The Insight Partners forecast predicts significant growth in the bariatric surgeries market, projecting an increase from $8.5 billion in 2022 to $27 billion by 2030, with a compound annual growth rate of 15.8%. It’s important to note that when this forecast was published, GLP-1 drugs had not yet gained widespread popularity. The projections were likely based on the anticipated rise in the number of obesity patients. The current landscape, with the prominence of GLP-1 drugs, may impact the actual trajectory of bariatric surgeries, potentially resulting in a slower growth rate than initially anticipated.

I have no doubt that bariatric surgeries generated significant demand for Intuitive Surgical’s da Vinci systems in the past. However, it is more likely that the growth in demand will decelerate in the near future.

Financial Review

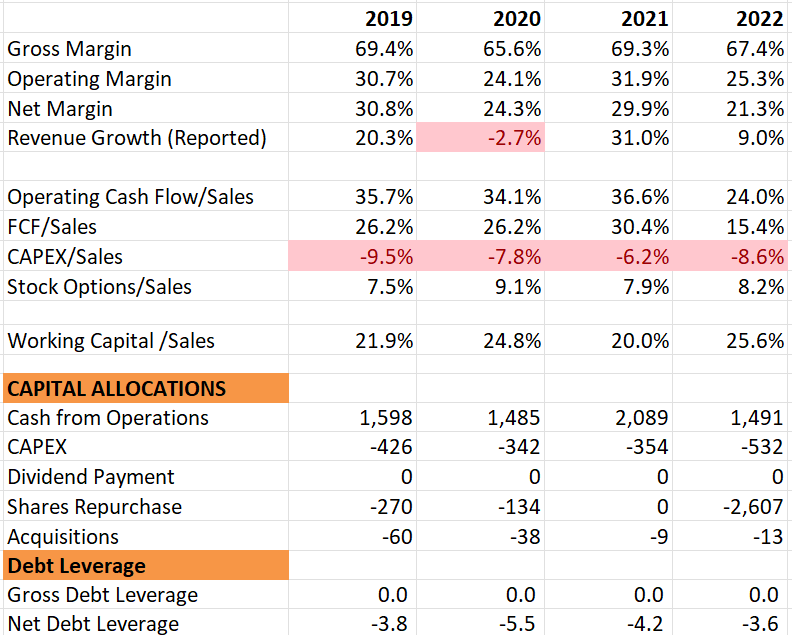

Historically, Intuitive Surgical has delivered impressive growth and maintained a strong margin profile, with both revenue and adjusted profits growing at mid-teens on average. The company boasts a super-strong balance sheet without any debt. In Q3 FY23, they ended with $7.5 billion in cash and equivalents. Most of their cash was allocated to R&D and sales/marketing, and they repurchased $2.6 billion of their own shares in FY22. Overall, I believe they possess a very strong financial profile and operate as a growth-oriented company in the healthcare sector.

Intuitive Surgical 10Ks

Valuation

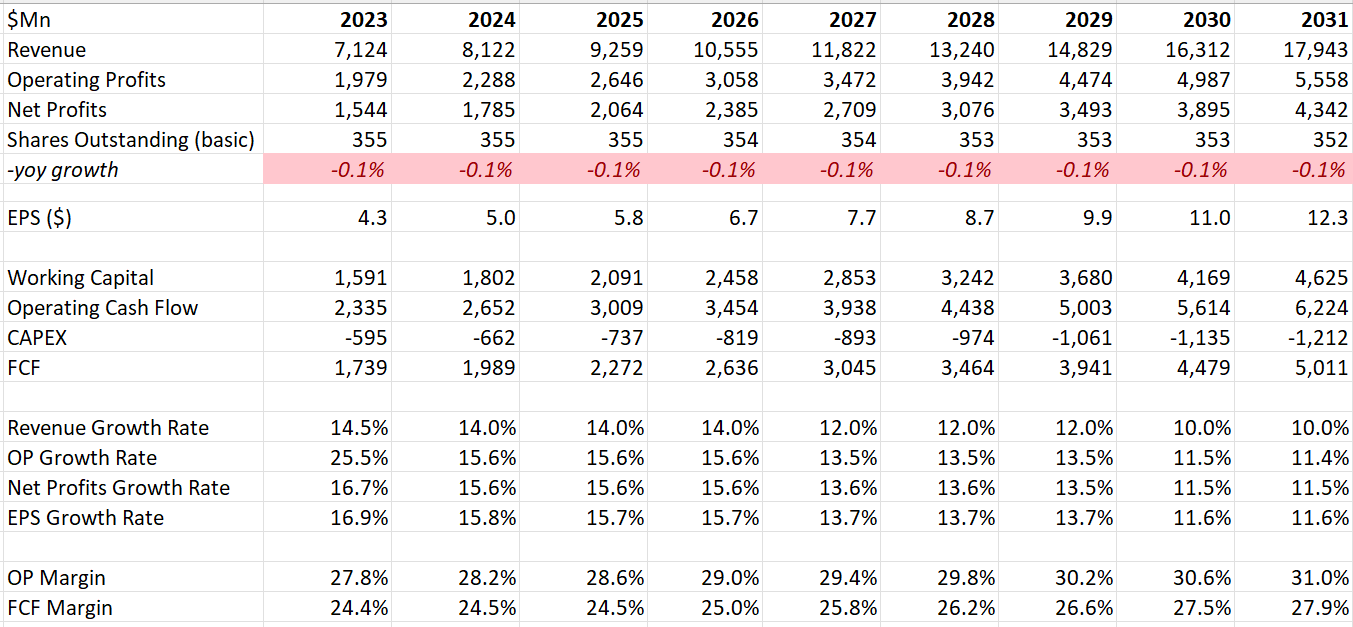

As they have already pre-announced their Q4 FY23 earnings, there won’t be any significant surprise when they officially release their quarterly results on January 23. My FY23 assumptions align with their guidance. For normalized growth, I assume they can deliver 14% revenue growth in the near term, gradually decelerating to 10% over time as their revenue base expands. Margin expansion is expected to be driven by operating leverage and a moderation of R&D spending over time. It’s worth noting that their operating margin is notably high compared to other medical device companies, owing to their innovative products and leadership position in their end-market.

Intuitive Surgical DCF – Author’s Calculation

The model employs a 10% discount rate, 5% terminal growth rate, and a 23% tax rate. Based on these parameters, the calculated fair value is $200 per share.

Key Risks

Product Lease: As the da Vinci system from Intuitive Surgical is relatively expensive, some hospitals opt to lease it rather than purchase outright. Leasing constitutes approximately 40% of the total systems placed. Hospitals retain the option to terminate leasing contracts, posing potential financing risks for Intuitive Surgical. However, I believe that adopting the leasing business model is a sensible strategy for the company.

Incoming Competition: Intuitive Surgical has maintained an almost monopolistic position for years, with Medtronic (MDT) and J&J (JNJ) now entering the field by developing their own robotic surgery machines. Medtronic’s Hugo Robotic-assisted surgery system obtained European CE Mark approval in 2021, and they are currently engaged in a U.S. trial. Consequently, competition is inevitable; it’s just a matter of how soon.

Conclusion

Despite my positive view on the company’s business and market leadership, I believe the stock price is currently overvalued. Additionally, the uncertainties associated with the company’s operations in China and the anticipated decline in demand for bariatric surgeries contribute to a less favorable outlook. Consequently, I am initiating a ‘Sell’ rating with a fair value of $200.

Q2 2024 Earnings Call Transcript")