Justin Sullivan/Getty Images News

Cereal legend General Mills, Inc. (NYSE:GIS) has had a tough go of it in the past several months. The pandemic brought staples producers to the fore, as they had massive pricing power amid shortages and rampant inflation. However, that led to unsustainable share price gains in many of those companies, and General Mills was certainly one of those in my view.

For the bulls, the good news is that GIS stock has been absolutely obliterated since the peak last May, all while the major indices are knocking on the doors of new highs. But is that enough? I’m not so sure.

Assessing the damage

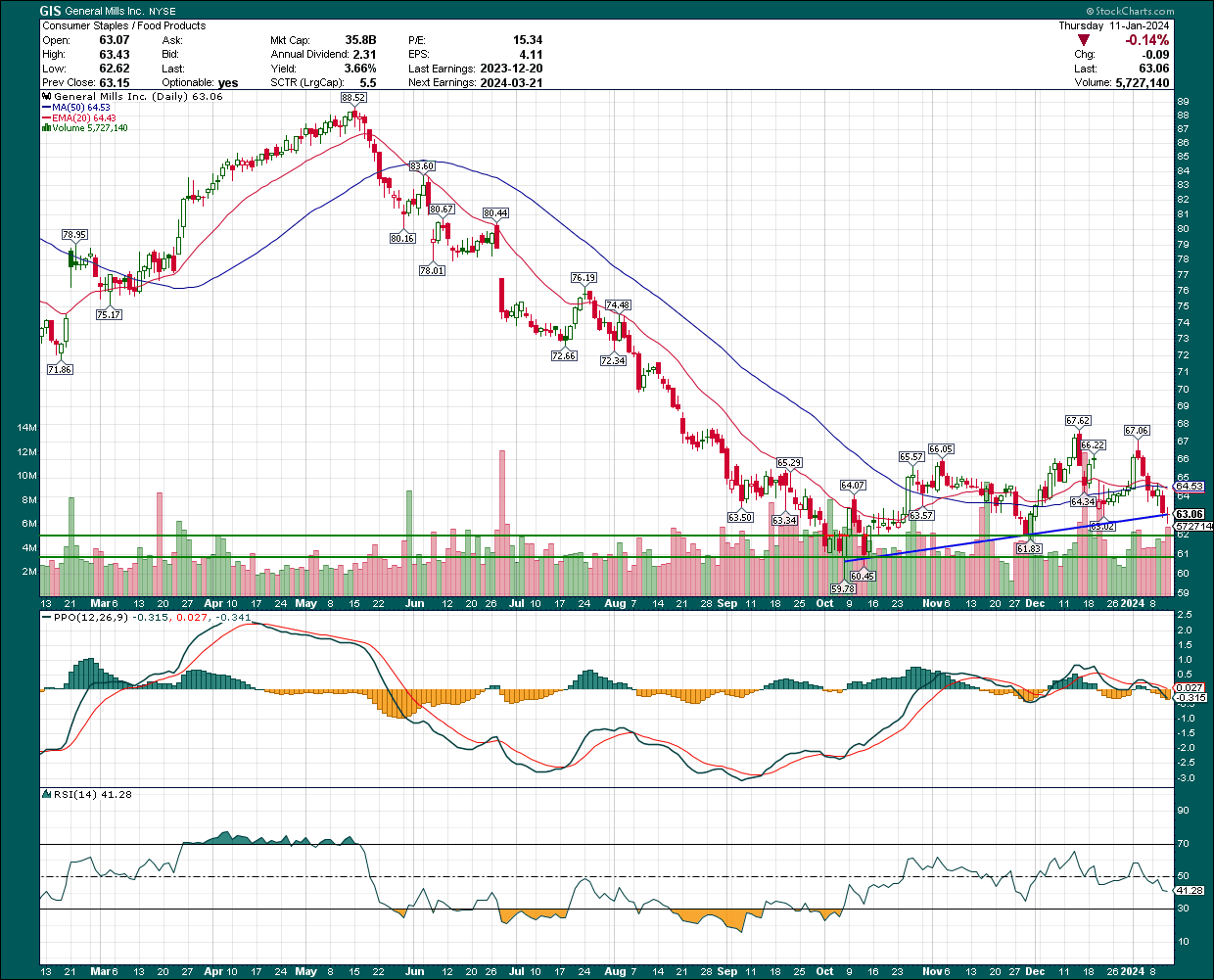

Let’s first take a look at the GIS share price chart to get a sense of the magnitude of the selling we’ve seen. The downtrend here is epic as there were very few bounces, just consistent selling and very little buying pressure.

StockCharts

The downtrend appears to have ended a couple of months ago, and right now, the bulls are being tested on trendline support right at $63. We’ll see what happens, but if that fails, there are two more lows – $62 and $61 – that could arrest any further declines in the stock. I will say that if the $61 level fails, look out below, but right now the risk/reward for longs is pretty good based on these levels in the near-term.

The problem that General Mills has is that it’s in an industry that has been completely ignored by Wall Street for months.

StockCharts

Food products have underperformed the S&P 500 (SP500) by 25% since May. Money has rotated out of the sector over and over again, and unless that changes, stocks like General Mills are going to struggle. For that reason, I don’t see any kind of meaningful recovery rally in the stock anytime soon.

Fundamental headwinds persist

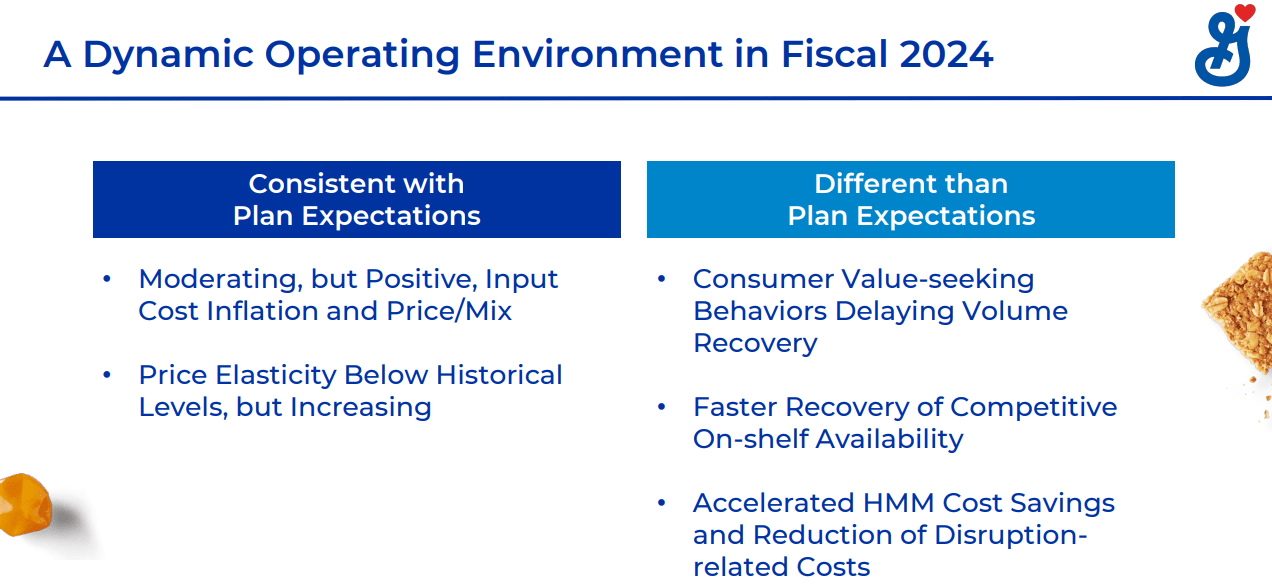

Demand for General Mills’ products is largely stagnant given it sells a lot of consumer staples. That’s a good thing during recessions, but also means growth is generally pretty modest. The problem is that not all is going to plan so far this fiscal year.

Investor presentation

The company is seeing moderating pricing power, and increasing price elasticity among consumers, meaning that consumers are becoming increasingly sensitive to higher prices. In practice, that simply means more customers are choosing value over brand loyalty.

On the right side of the above, we can see that consumers are seeking value, which is a result of that price elasticity. Given General Mills is the premium player in the segments in which it competes – as opposed to private label versions of its products – this is simply not good.

The most recent inflation data showed further moderation in many of the categories General Mills competes in, further cementing that pricing power is likely a thing of the past. With that, I believe General Mills is facing an uphill battle on both revenue and margins.

Investor presentation

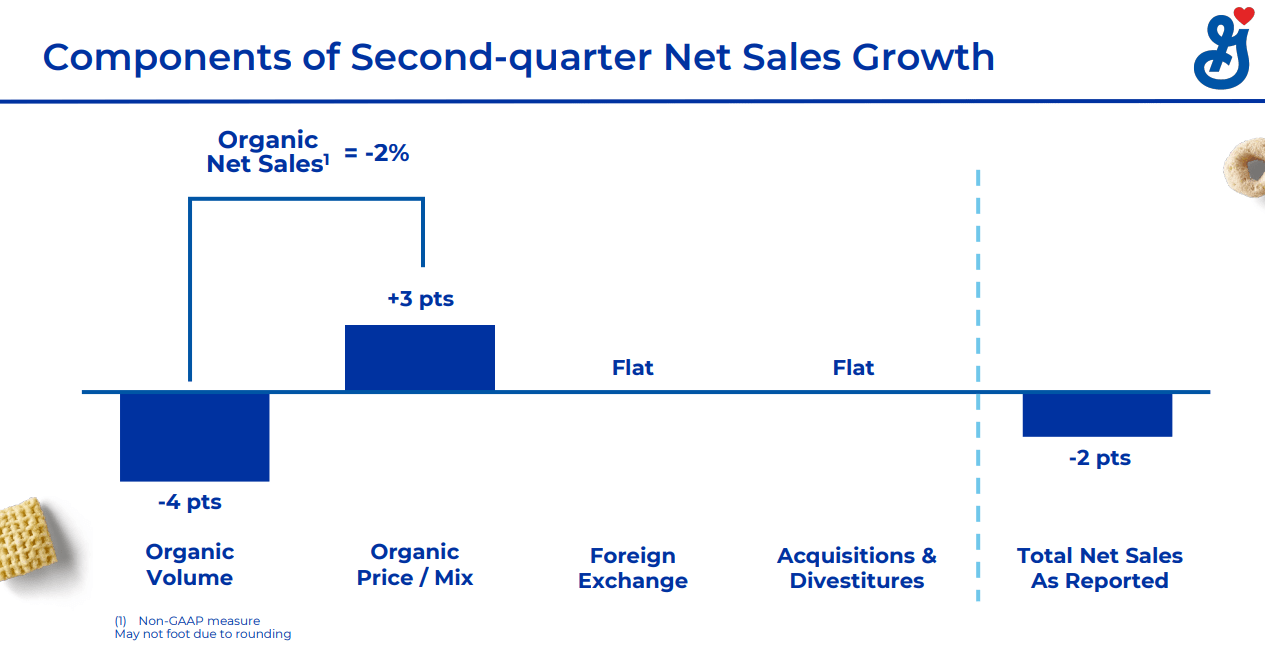

The fiscal second quarter showed organic volume falling 4% year-over-year, which is a big number for a company that makes staples. Pricing and mix was +3%, but if consumers seek value, have greater price elasticity, and inflation in food categories continues to moderate, how in the world is General Mills going to keep that up? If it doesn’t – that’s my base case – we’re looking at weak volume that won’t be offset by stronger pricing any longer.

Management has been boosting margins via a few levers, including logistics efficiency, manufacturing savings, and reduced levels of excess inventory. Those are noble goals and the company is delivering, but as with any cost-savings program, there a limits to its effectiveness.

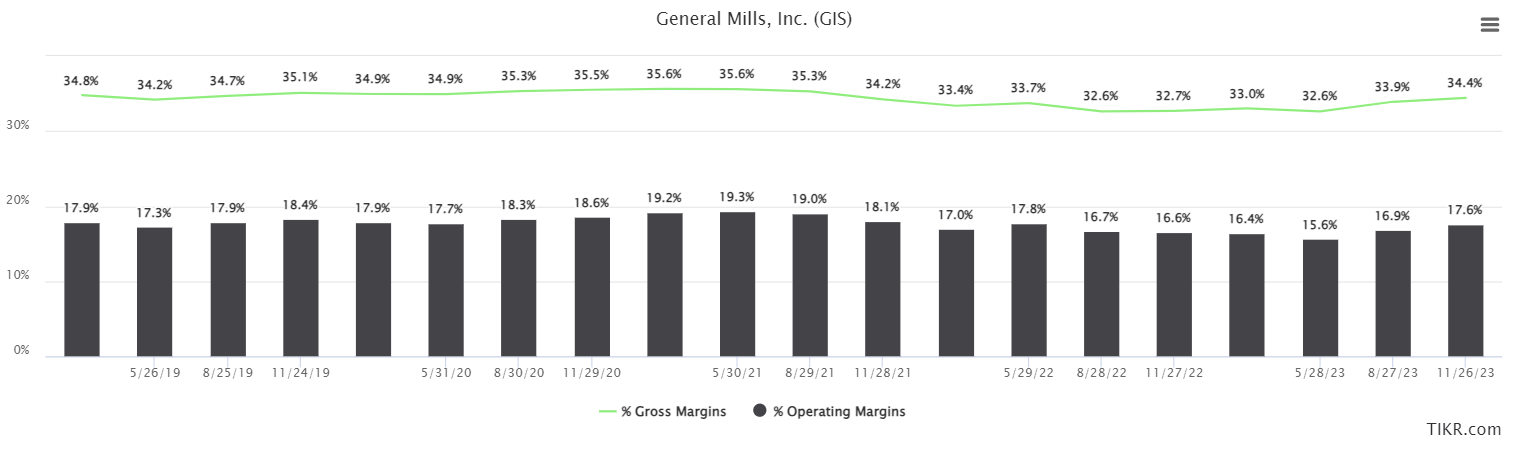

In addition, even with these savings and two or three years of nearly limitless pricing power, margins continue to trend below historical levels.

TIKR

This is a trailing-twelve-month (“TTM”) look at gross and operating margins to illustrate this, with both moving up recently. That is not necessarily a surprise given the pricing power the company has seen, but if I’m right that those pricing power characteristics are fading, I struggle to see further gains in the above. That will have a direct impact on General Mills’ ability to boost EPS.

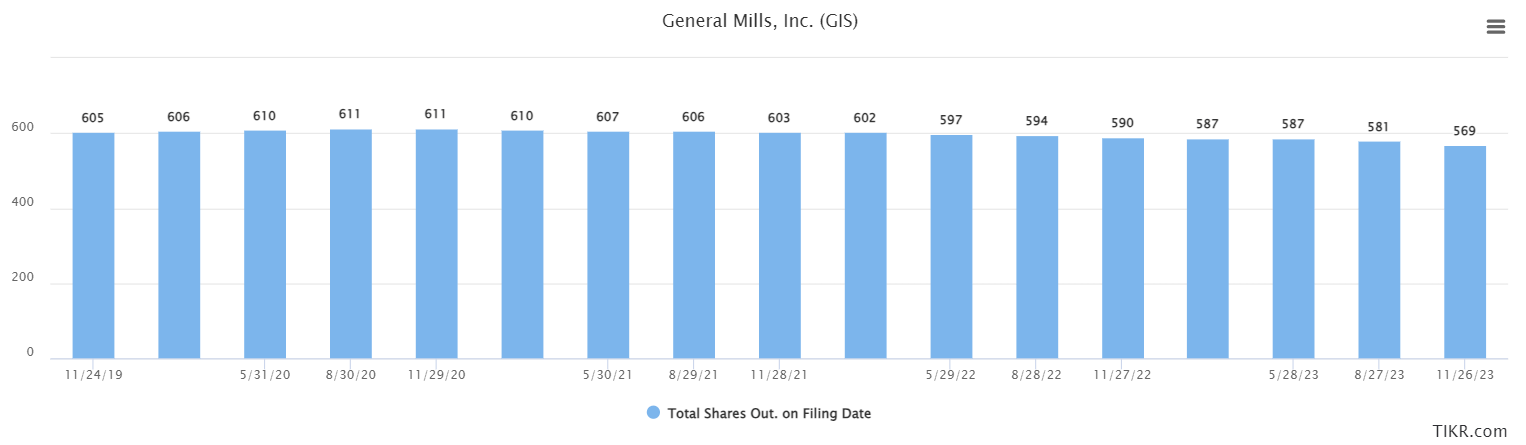

The final piece of EPS growth apart from revenue and margins is the share count, and General Mills has been gradually boosting its share repurchases as the stock has fallen.

TIKR

Share repurchases have been modest in the past few years but have picked up steam quite recently. This has the chance to offset some of the fundamental weakness I called out if it continues, so that’s a net positive for EPS growth.

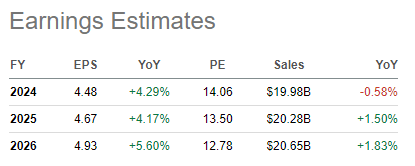

If we add all of this up, here’s the current slate of estimates for revenue and EPS.

Seeking Alpha

Revenue growth is expected to be quite modest – under 2% annually for the foreseeable future – but slightly better EPS expansion. These estimates seem reasonable if the company continues to buy back shares at 2% or 3% annually, but it is my view that revenue and margins will contribute very little to EPS growth in the coming years.

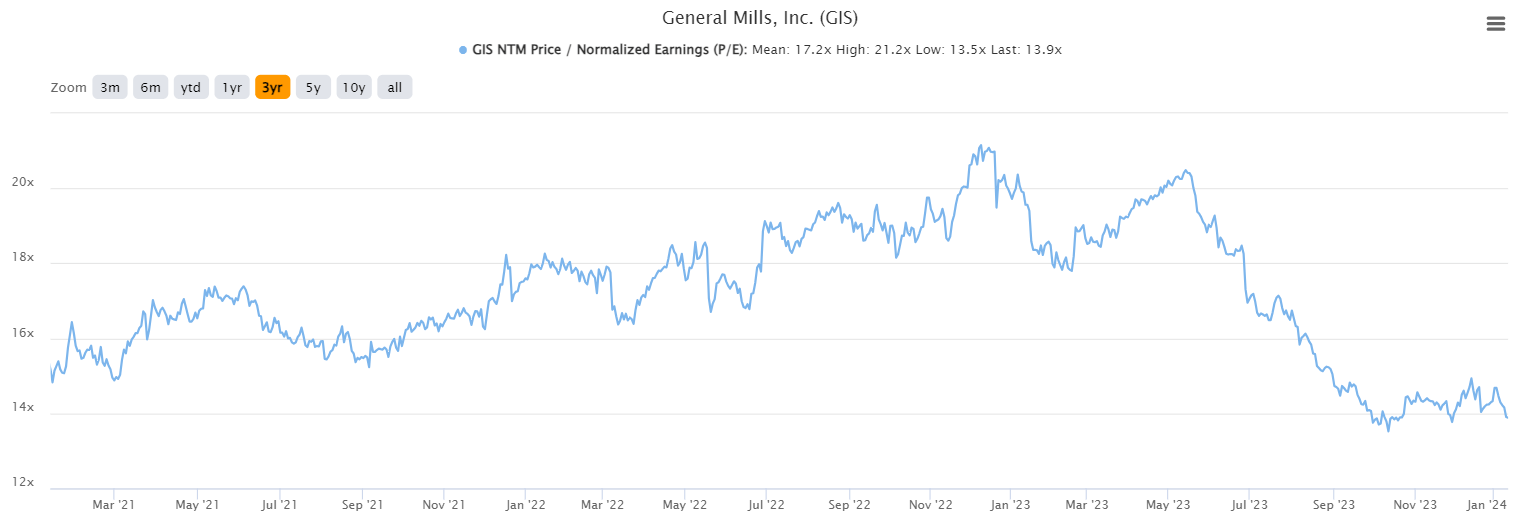

Cheap, but it is cheap enough?

The answer to that question is largely in the eye of the beholder, but there is no denying the stock is a lot cheaper than it has been.

TIKR

It goes for just 14X forward earnings at the moment, well off from the high of 21X, and meaningfully lower than the 3-year average of ~17X. The thing is that forward P/E ratios are largely dependent upon expected growth, and General Mills has little of that at the moment.

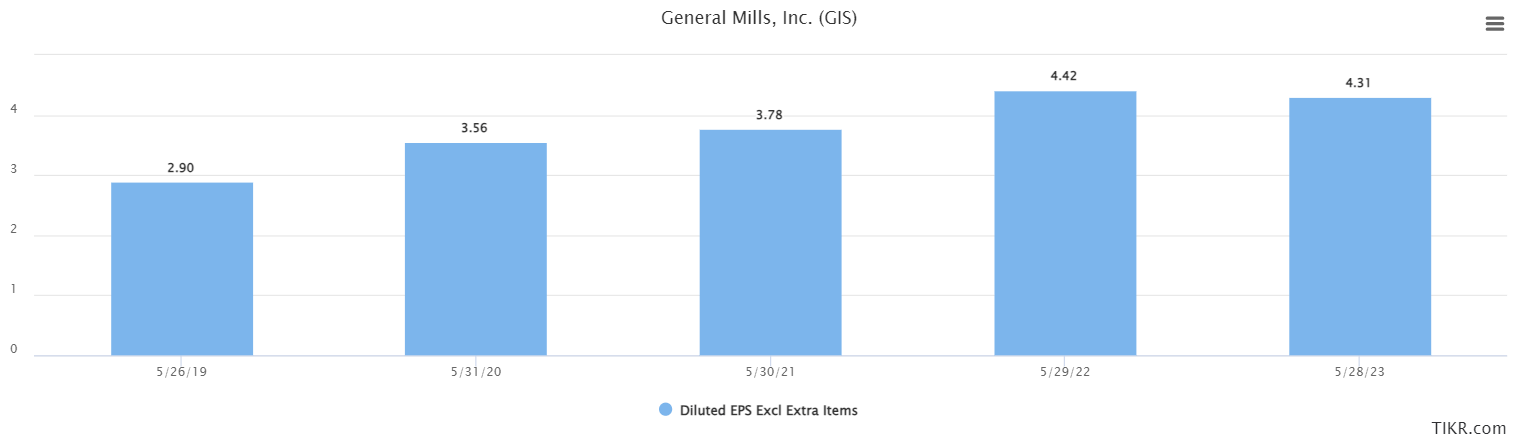

TIKR

EPS soared from 2019 to 2022, but it’s clear the tailwinds that drove that growth have passed. We saw lower earnings last year, and modest projected growth this year. With this context, a declining valuation makes perfect sense to me. So is the stock cheap? Yes. Does it deserve to be cheap? Undoubtedly, yes. For me, the valuation is fine, but not enough to sway me off of my general caution around the company’s fundamental picture.

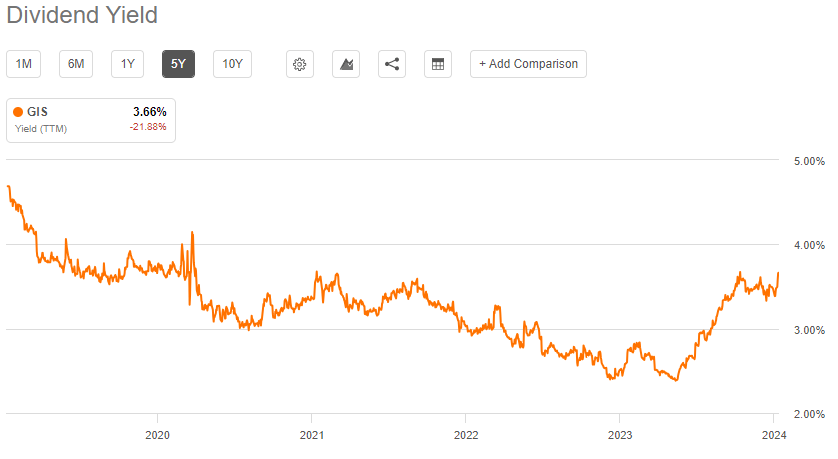

Finally, we can use the GIS dividend yield as a valuation tool given General Mills’ longstanding reputation as a strong dividend stock.

Seeking Alpha

We see a ho-hum picture here as well, as the yield is mostly in the middle of the five-year range. While it’s a much better yield than it was, just like the valuation, it’s not enough to sway me.

The bottom line is that this stock getting pummeled was overdue. The thing is that given the fundamental issues I’ve called out, I don’t think General Mills, Inc. stock necessarily is cheap enough to buy; I think it has simply been reset based upon the new normal of lack of pricing power and the issues that brings.

For that reason, I’m placing a sell rating on General Mills, Inc. stock. Money has been flowing out of the sector, and flowing out of General Mills shares. I don’t see an upside catalyst anytime soon, and I think you’re better off in other sectors of the market.

Q2 2024 Earnings Call Transcript")