skynesher

Insurance stocks bottomed out relative to the S&P 500 last summer. Financials in general were a notable laggard in 2024 despite a year-end rally. With interest rate volatility that appears to be easing, the group hopes to find some stability in 2024 with bigger profits given more stable and higher interest rates today compared with the previous cycle.

Despite some industry tailwinds, I am downgrading shares of Unum Group (NYSE:UNM) from a buy to a hold on a weaker earnings outlook this year and softer momentum trends. I see the stock as less attractive today, but its yield and EPS growth in the out years are possible upside catalysts. You can view my previous analysis of UNM here.

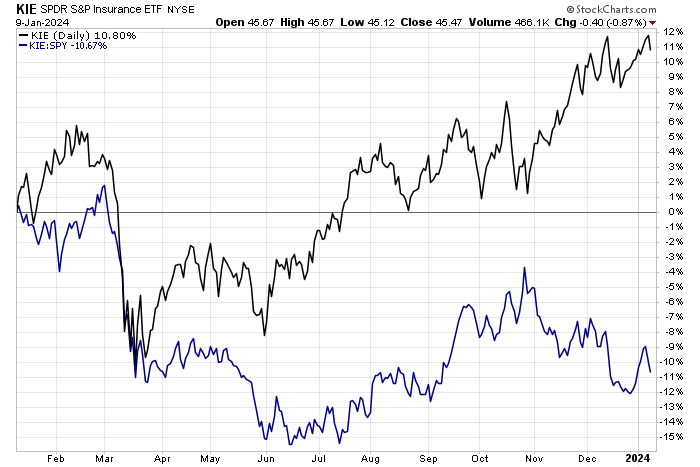

Insurance Stocks Trying to Hold Their Mid-2023 Relative Lows

Stockcharts.com

According to Bank of America Global Research, Unum is a leading provider of disability income insurance and ranks among the world’s leading special risk insurers. Unum has a strong market share in the U.S. and U.K. Unum has a large legacy book of long-term care (LTC) and individual disability but has put these businesses in runoff. The company distributes via captive sales representatives, brokers, and sales consultants.

The Tennessee-based $8.8 billion market cap Life and Health Insurance industry company within the Financials sector trades at a low 5.9 forward non-GAAP price-to-earnings ratio and pays an above-market 3.2% dividend yield as of January 9, 2024. Ahead of earnings due out later this month, shares trade with a moderate implied volatility percentage of 25% while short interest on the stock is low at 1.4%.

Back in October, UNM reported a mixed set of Q3 results. Quarterly non-GAAP EPS of $1.94 beat the Wall Street consensus forecast of $1.91 but revenue of $3.1 billion, up just 4.4% from year-ago levels, missed by $20 million. The firm demonstrated solid operating performance, but softer sales were seen in its Colonial insurance segment and its International slice. There were also concerns about the health of its long-term care business.

A bright spot was the margin story in its group disability and life businesses. What drove shares lower was a significant $369 million charge in its LTC unit. The bulls can point to the charge stemming from an accounting change in the LTC assumptions, which analysts at Evercore ISI claim is more “accounting noise,” clouding what was otherwise a strong quarter.

Key risks for Unum include further weakness and any impairments in its LTC business, leading to lower overall margins and profitability. A continued move lower in interest rates off the highs in October could also be a headwind for its bottom line. Regulatory issues could also arise given the industry – any pressure there could harm the currently high dividend yield, though that is not expected. Its former COO Michael Simonds resigned earlier this month, but no reason was given.

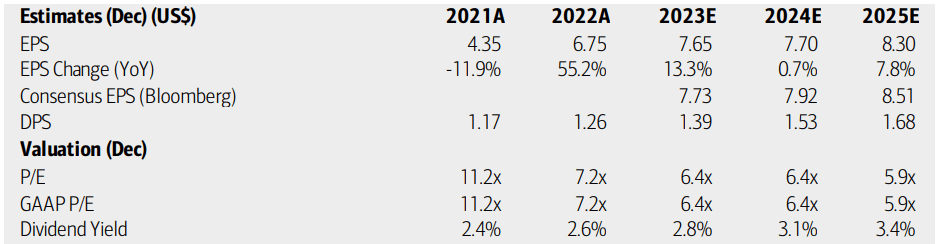

On valuation, analysts at BofA see earnings growth slowing this year after 2023’s robust gains. Per-share profits are then expected to accelerate in the out year. The current consensus forecast, per Seeking Alpha, shows 25% operating EPS growth for 2023 and 7.3% growth in 2025. Top-line growth is seen between 3% and 4% over the next two years. Dividends, meanwhile, are forecast to increase at a steady and strong rate over the coming quarters, potentially lifting the dividend yield closer to 4% if the share price remains under $50.

Unum: Earnings, Valuation, Dividend Forecasts

BofA Global Research

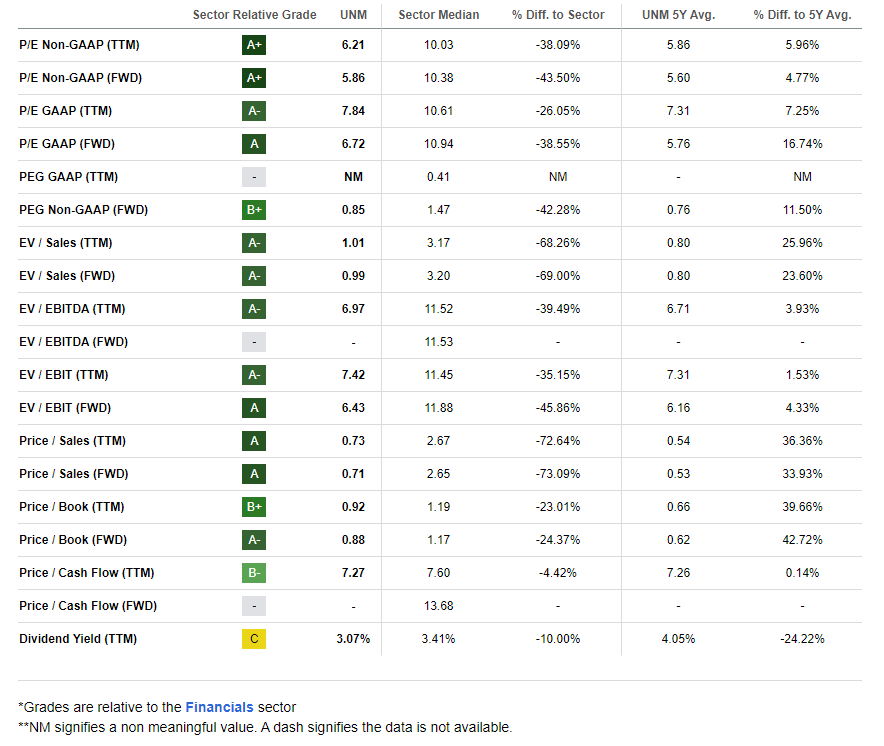

If we assume a 6x earnings multiple, slightly below some of its life insurance peers and near UNM’s long-term average, and apply a normalized operating EPS figure of $7.8, then the stock should trade near $47. Risks regarding its long-term care exposure may pressure the multiple, so a below-sector P/E is warranted. Still, valuation metrics relative to its sector are compelling, while pricing versus UNM’s history are less attractive.

UNM: Priced Cheaply But Not Compared With Its 5-Year Average Multiples

Seeking Alpha

Compared to its peers, UNM features a solid valuation, while its growth history and prospects appear healthy. With robust profitability trends and a positive EPS revision history, UNM appears in a good position compared to the industry. But with EPS seen about flat this year, there are some headwinds. What has been weak lately, however, is its share-price momentum trend. I will detail key price points to monitor on the chart later in the article.

Competitor Analysis

Seeking Alpha

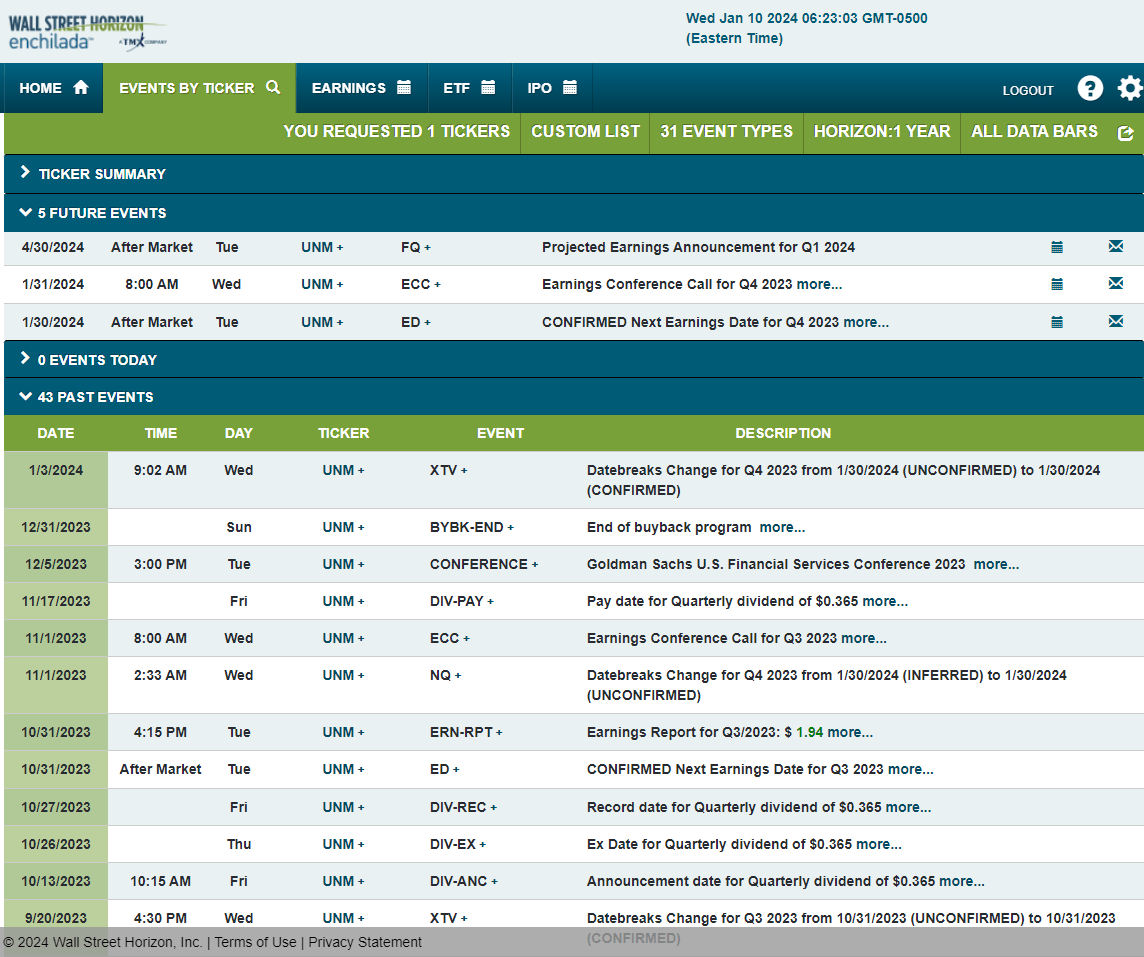

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q4 2023 earnings date of Tuesday, January 30 AMC with an earnings conference call immediately after the numbers hit the tape. You can listen live here. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

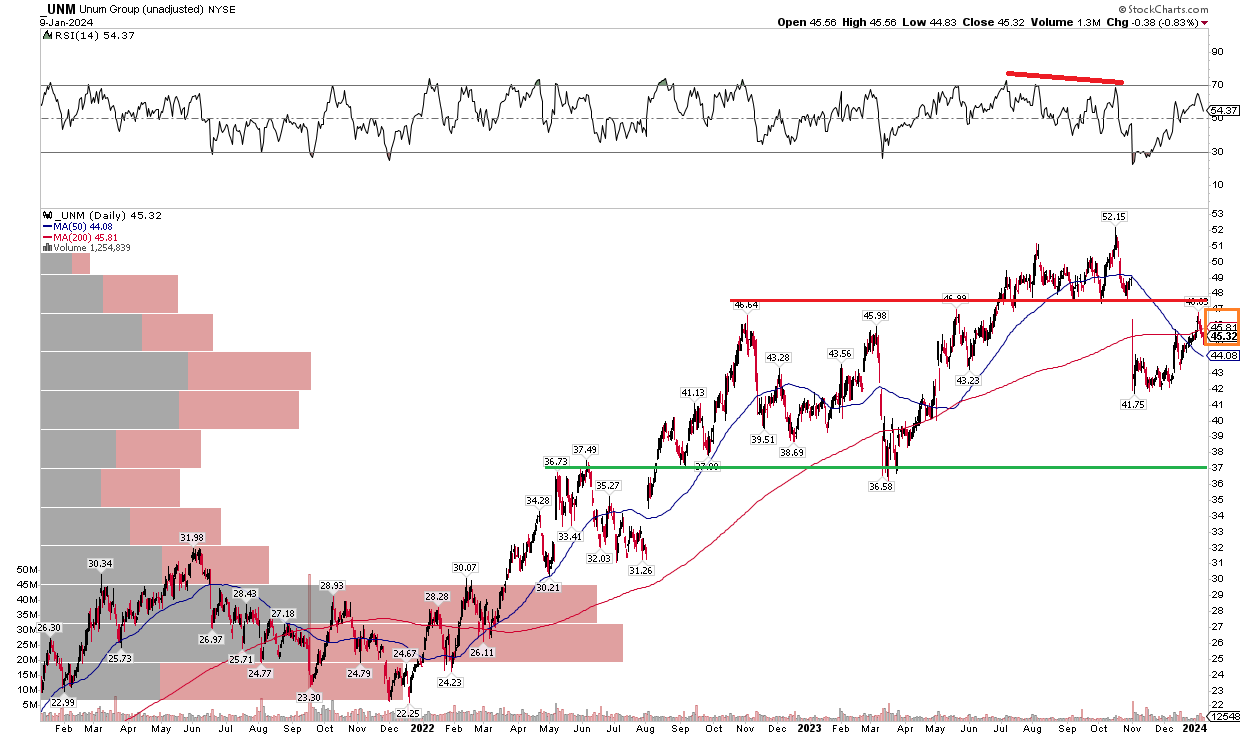

Back in Q2 last year, I outlined a bullish technical feature that, in my opinion, augured well for gains in the second half of 2023. That appeared to be playing out as Q4 got underway. Unfortunately, UNM broke down through key support at the $47 mark. That level had been resistance from late 2022 through mid-2023. Notice in the chart below that this bearish false breakout pattern came alongside a bearish RSI divergence. Technicians like to see price and momentum confirm each other. In this case, lower highs were being notched in the RSI oscillator at the top of the graph. The stock then plunged on an earnings-related move the day after its Halloween quarterly report. UNM also dropped under its 200-day moving average, which is now flat in its slope after trending higher for many months.

I see $47 as renewed resistance, while support is apparent in the mid to high $30s. I would like to see UNM rally back above the $47 line on strong momentum with improved volume. For now, the technical situation is less sanguine compared to what was seen last spring.

Overall, the technicals have turned less favorable, with UNM under important resistance.

UNM: Bearish False Breakout, Shares Under Key Resistance

Stockcharts.com

The Bottom Line

I am downgrading UNM to a hold from a buy. Recent performance has been weaker, and this year’s earnings outlook is less bright. Still, with a low valuation, there’s room for optimism if we see a rebound in some of its key financial metrics.

Q2 2024 Earnings Call Transcript")