JHVEPhoto/iStock Editorial via Getty Images

The TSMC Investment Thesis

Taiwan Semiconductor Manufacturing Company (NYSE:TSM) or most commonly referred to as TSMC is the heart of today’s economy. This is because semiconductors are now a key part of nearly every type of electronic device, from cars to smart phones. Most people are probably not aware that even appliances like refrigerators depend on this industry, and that the chip shortage affected 169 different industries.

It is therefore not surprising that the USA has introduced the Chips Act and that other governments are investing significantly in this sector. And the company that has by far the best set of advanced nodes is TSMC. However, given the historical obstacles to Taiwanese independence, the company is trading at an attractive valuation.

Does TSMC Have Any Real Competitors Or Are They Just Companies In The Same Market?

In my opinion, Samsung (OTCPK:SSNLF) is the only company that is somewhat competitive with TSMC, and even they are far behind in advanced chips and compete more by slashing prices on the less advanced chips. Samsung’s problem at the moment is that the yield of their chips is not satisfactory, as the 3nm chips are unfortunately just 60%. To threaten TSMC, however, it would have needed a yield of more than 70%. However, it is important to note that most of the published articles on yield rates are estimates from industry experts and not publications directly from the companies, so the yields should be taken with a grain of salt.

But as a result, TSMC’s market share in the advanced foundry market is a whopping 66% due to its reliable and high-quality semiconductors. However, TSMC also struggled with the 3nm chips, giving Apple (AAPL) the opportunity to negotiate prices for the chips used in the iPhone 15 Pro model. Nevertheless, Apple has already selected TSMC to produce the chips for the iPhone 16.

However, Samsung is an alternative to TSMC for 4nm and 5nm chips. But if Samsung wants to compete on AI chips in the future, then they need to be the leader on 2nm or 1.4nm. And I cannot see them overtaking TSMC in this advanced field as TSMC has such a big knowledge advantage and much larger capacity.

Intel, on the other hand, has the advantage that the U.S. and Europe desperately need a competitive semiconductor manufacturer. Therefore, the chips act money and various EU subsidies will most likely end up with Intel. Even Israel has already decided to start funding Intel. But even with unlimited resources, you cannot compete with TSMC’s years of experience and expertise. And I mean, if the reports are true, Intel has even outsourced some of its products to TSMC. This alone would be further evidence of TSMC’s competitive advantage.

TSMC’s advanced chips are essential for smartphones, laptops, automotive, artificial intelligence, HPC and more. In other words, the chip shortage crippled the automotive industry for a while, and so the previously unknown Taiwanese company became known to more people. And many are unaware of how many other companies depend on TSMC. Broadcom (AVGO), for example, gets 90% of its wafers from TSMC. NVIDIA (NVDA) and AMD (AMD) also rely heavily on TSMC. If TSMC were to stop shipping chips, the global economy would be in crisis.

Governments even agree that TSMC’s factories outside Taiwan will only produce less advanced chips such as 12/16nm and 22/28nm in order to ensure the supply of chips. In addition, they are likely to be more expensive than those made in Taiwan. That sounds like real pricing power to me. But Japan, Germany and the U.S. know that the demand is overwhelming and the barriers to entry are high to produce chips at or near TSMC’s standard.

And I think the number of industries that are dependent on TSMC’s product will only increase in the future because we are probably just at the beginning of the cycle.

TSMC’s Metrics and Balance Sheet

Most of the time I see people talking about TSMC’s strong gross margin, but I think the net income margin is even more impressive. This is a company that many people have said is in a capital intensive industry and they have a net income margin of over 40%. That is really remarkable. Even as competitors try to compete on price, TSMC still has a lot of room to be highly profitable. Just the difference in wages between the Western world and Taiwan is a huge competitive advantage. TSMC could probably match any competitor’s selling price if they wanted to. But because their products are so much better, they do not need to engage in such a price war.

They also have an impressive balance sheet. $48 billion in cash and only $29 billion in long-term debt. So if they wanted to, they could pay off all their debt at any time. And even net income in December 2022 was greater than LT debt. So LT debt is less than 1x net income. Again, a sign of strong financial position. And the Q4 results coming out later this month are likely to show that this will be the case in 2023 as well.

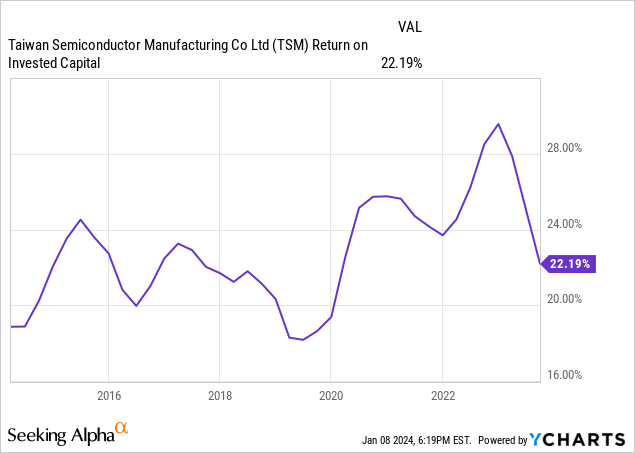

TSMC’s Capital Allocation And ROIC

TSMC’s high ROIC further strengthens the case that the company has strong competitive advantages as they are able to generate well above-average returns on capital. Since TSMC has low interest expenses, its cost of debt is really low at only 1.5%, but its cost of equity is about 11%, resulting in a WACC of about 10%. So we have an extremely strong ROIC-WACC spread of 12% right now.

Investments in R&D, which amount to around 8% of sales, are therefore bearing fruit. And if we look at a simplified version of owner earnings, which is dividend yield + EPS growth, we get the following figure.

Another strong figure that should please existing shareholders. And with a dividend growth rate of 12.61% per year since 2012, the company is also a relatively good dividend growth stock.

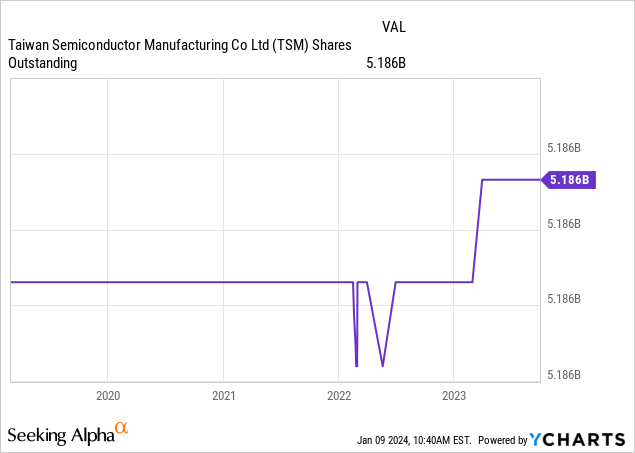

Another thing that should please existing shareholders is that the company has had almost the same number of shares outstanding for the past 5 years. No excessive SBC and no shareholder dilution. A pretty sweet situation.

TSMC’s Valuation

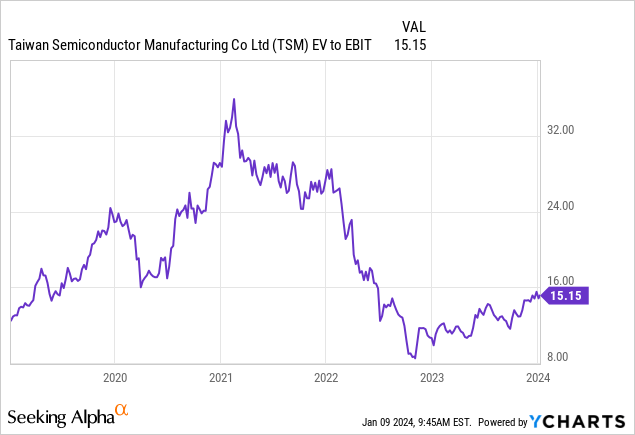

I like to use the EV/EBIT multiple because it is relatively similar to the pre-tax multiple used by Warren Buffett, and most of Berkshire Hathaway’s (BRK.A) big investments have historically been in the 13x range. As a result, TSMC’s 15x multiple is by no means overpriced. Rather, it is fairly valued with the potential to be quite attractively valued. And the 5-year EBIT CAGR is 20.58% and the 10-year CAGR is 16.84%. These are growth rates that should normally justify a higher multiple.

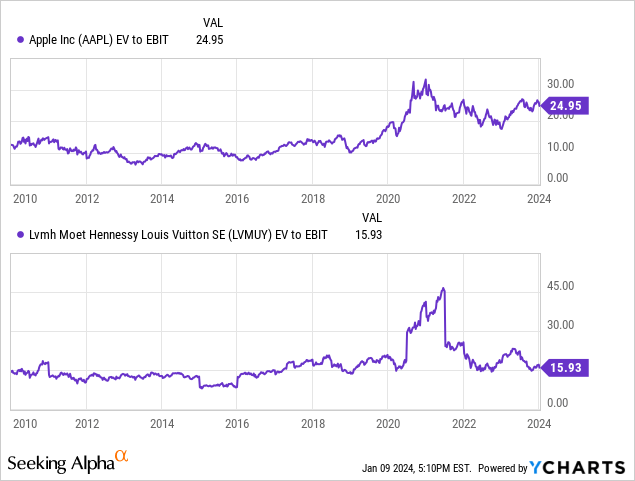

Apple and LVMH (OTCPK:LVMHF), two companies of similar quality, were both excellent investment opportunities that gave shareholders a lot of pleasure in the following years when they were available at 15x EV/EBIT a few years ago. Apple has a total return of 2,765.48% since 2010 and LVMH has a total return of 839.56%, both easily beating the S&P 500 (SPY) over that period from a similar starting position as TSMC today.

Risks

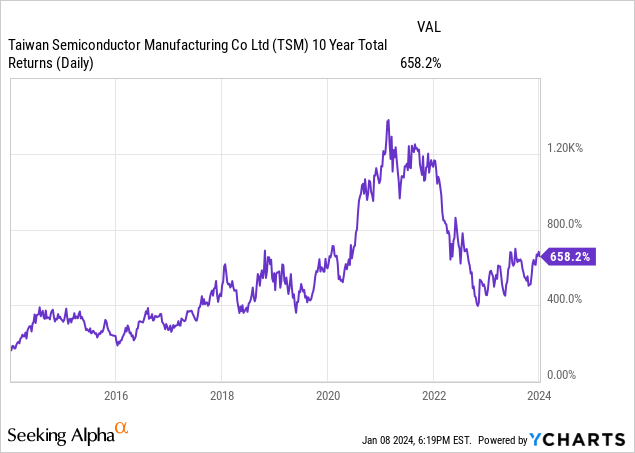

The obvious risk is the political and geopolitical risk combined with trade tensions. But this risk has been around forever, and investors who took the chance have been handsomely rewarded over the past 10 years, as we can see in the chart above. As a result, this situation has created a tremendous opportunity for investors. If this were an American company, it would probably be trading at 2 to 3 times the multiple it is now. And no one can say with 100% certainty how this situation will play out, but since this is a known risk, it is likely that sufficient precautions have been taken in the event. It is the risks that are ignored that are often the cause of the most damage.

Another risk that has become somewhat smaller is concentration risk. In FY21, the 10 largest customers accounted for 74% of net sales and the largest customer alone accounted for ~25%. However, due to the shift to HPC, the top 10 accounted for only 68% and the largest customer only 23% of net revenue in the most recent 20-F. This trend is likely to continue.

In addition, and this is something I have not seen talked about much, is the risk that TSMC gets its raw materials, which account for 95% of its wafer needs, from only six different companies. And those are two Taiwanese companies, two Japanese companies, and one each from Germany and Singapore. So even a company like TSMC depends on other companies. And also ASML Holding N.V (ASML) is really important for the smooth flow in the production + design of semiconductors.

Conclusion

An interesting fact is that Saudi Arabia controls about 12% of the oil market, which has fueled the rise of the global economy for decades and provided the country with considerable wealth. TSMC, meanwhile, has a 66% market share in what could be the driver of the global economy for decades to come. So I think the importance of this company cannot be emphasized enough. And the politicians of the world know it too, as we can see by their actions. But shockingly, many investors do not know about this company and its reputation. And even if they do know about it, they are afraid to consider it as an investment because of all the things that are going on around it.

And anyone can see that TSMC is attractively valued because of these factors. The big question now is what happens next? And there are different scenarios, but I think the most likely one is that there will be a peaceful resolution. Both the U.S. and China do not want a conflict. A peaceful resolution benefits both, and I think China understands that because they make decisions that are best for their country and their people.

Q2 2024 Earnings Call Transcript")