JHVEPhoto

Investment action

I recommended a hold rating for Intuit (NASDAQ:INTU) when I wrote about it the last time, as I expected headwinds from the macro environment to impact INTU’s core customer base – small businesses and consumers. Based on my current outlook and analysis of INTU, I recommend a buy rating. My change in rating is primarily due to INTU performing much better than I expected in 1Q24, showing that it is not heavily impacted by the macro environment (which was my concern). Not only that, INTU also showed that it is making more inroads into the mid-market, paving the way for it to further penetrate the upmarket. All of these led me to believe that INTU can accelerate its earnings growth to the high teens range.

Review

INTU did surprisingly well in 1Q24, despite my concerns about the macroeconomic conditions impacting small businesses. Revenue grew 14.7% to $2.98 billion, beating consensus estimates by 370 bps. Pro-forma [PF] EBIT also beat the consensus estimate, where INTU reported $960 million in EBIT and a 32.2% EBIT margin vs. the consensus estimate of $769 million and a 26.7% margin. Consequently, PF EPS saw $2.47, beating the consensus estimate of $1.98.

I now believe INTU is a much more resilient business than initially thought. To give a recap, my view was that small businesses are extremely prone to the macro cycle, and since INTU mainly targets these businesses, it would continue to face growth headwinds if the economy does not recover. After assessing the INTU 1Q24 results, I came to the realization that small businesses are more durable than I expected. For context, Q1 revenue for INTU Small Business Group was up 18% year over year, which was higher than consolidated business growth. Despite the fact that online services rather than the core QuickBooks Online subscriptions drove outperformance, this demonstrates that INTU is capable of selling a wider range of solutions to its substantial customer base.

I should have known better than to presume that the macrocycle would affect all INTU small businesses. During the call, management brought up this dynamic, saying that small and medium-sized business customers are doing well overall, but that it all comes down to factors like customer size, operating history, and industry exposure. My opinion is that inflation, rising rates, and a tight labor market are likely to continue negatively impacting small businesses, but the impact will be more skewed toward those operating in discretionary industries. Given INTU’s diverse portfolio of small businesses, the impact of the current macro situation is more manageable than it appears.

Macro matters aside, INTU’s bill pay product has also seen very good traction that I expect to continue. As background, the goal of the bill pay product is to give clients a powerful, simple, and intuitive way to handle accounts payable and business-to-business transactions. There are two implications for this successful launch. Firstly, it brings another revenue stream to INTU. Secondly, which is the more important aspect, is that it paves the way for INTU to penetrate further into the mid-market segment. During the call, management called out that its mid-market customers are choosing the paid subscription offering at around twice the rate of non-mid-market customers. This clearly shows INTU gaining more traction with larger customers, making the case for INTU to go upmarket more and more plausible.

Valuation

Author’s work

I am revising my hold rating to a buy rating as I now see INTU as a much more resilient business than I initially believed. Previously, because of my concern about the macroclimate, I did not give management the benefit of the doubt that the top line can grow to high teens. 1Q24 results proved me wrong, and I now believe that INTU can accelerate its earnings growth through FY26 as:

- Small business’s performance is much more durable.

- Macro conditions are much better today than the last time I wrote about them.

- INTU continues to find success in penetrating the upmarket.

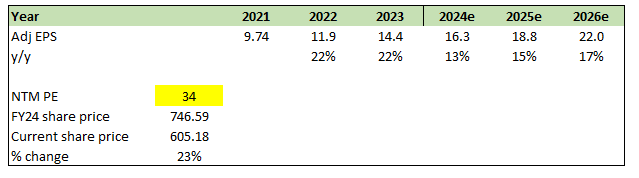

I have adjusted my model to use adj EPS as the core assumption, as this is a metric that management has guided. I expect adj EPS to accelerate by 200bps each year, from 13% in FY24 to 17% growth in FY26. Regarding valuation, I have stepped up my assumption from 30x to 34x because of the better earnings growth outlook. Previously, I thought that INTU should trade at ~30x forward PE because it was growing in line with its historical low-teens growth rate. Now that I expect growth to be better, I think INTU deserves to trade at a premium compared to its trading history.

Risk and final thoughts

Products and services targeted at consumers that assist with tax filing make up a substantial chunk of INTU’s revenue. Over the years, more and more people have turned away from tax preparation services and manual options in favor of do-it-yourself approaches, with TurboTax being a prime example. If this trend were to diminish, stop, or turn around, it would probably have a negative impact on INTU’s growth and profitability.

I have revised my rating for INTU from hold to buy. Contrary to earlier concerns about macroeconomic impacts on small businesses, INTU showcased remarkable resilience, outperforming expectations with 14.7% revenue growth, surpassing consensus estimates across EBIT, margins, and EPS. INTU’s bill pay product traction in the mid-market was also a very positive update as it indicated that INTU was making good progress in penetrating the upmarket – which should extend the business growth runway.

Q2 2024 Earnings Call Transcript")