Trevor Williams/DigitalVision via Getty Images

The Williams Companies (WMB) is an American, Oklahoma based energy company. The company, with a market cap of more than $40 billion, has major natural gas processing and transportation assets. As we’ll see throughout this article, the company’s impressive assets will enable the company to continue driving additional shareholder returns.

Williams Companies Overview

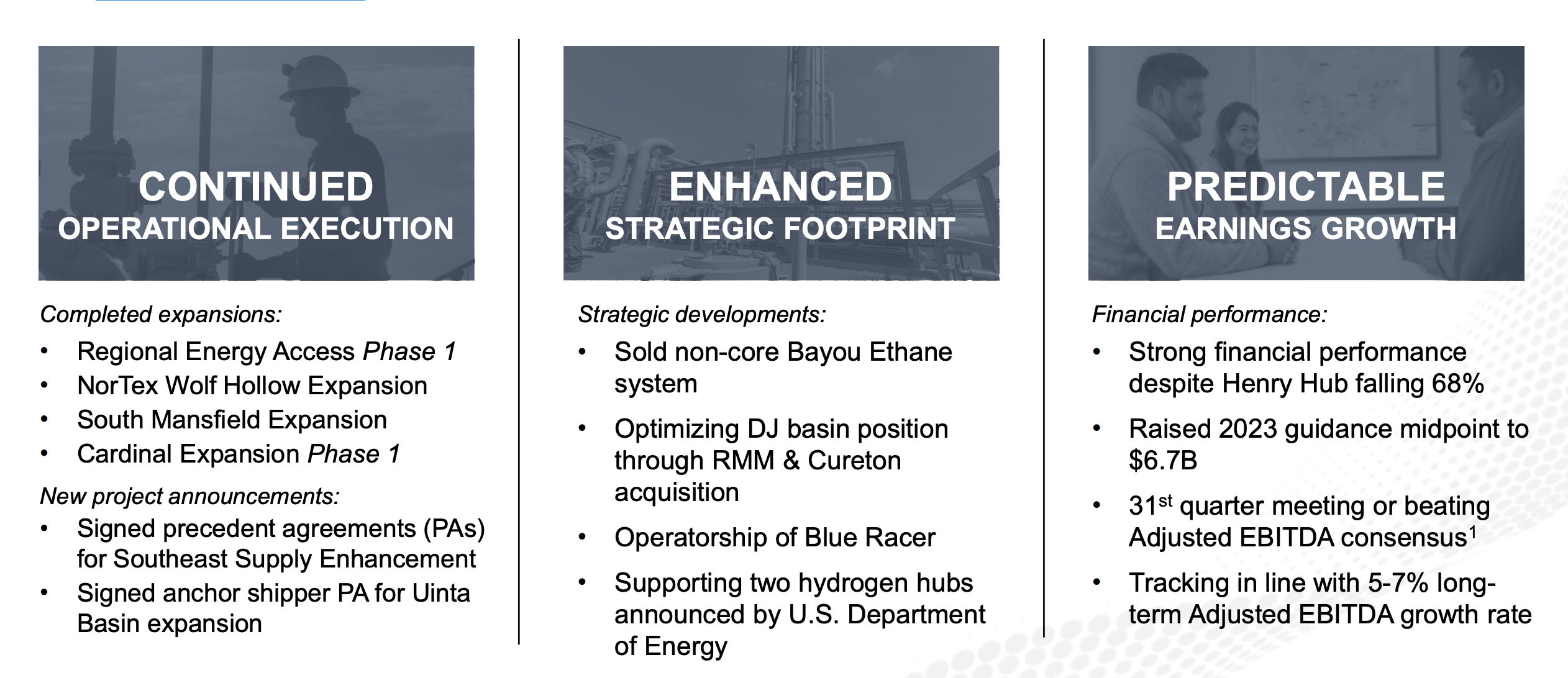

The company has a strong portfolio of assets, and has continued to perform well.

Williams Companies Investor Presentation

The company has properly completed a number of expansions and has announced several additional expansions. At the same time, the company has managed to improve its strategic footprint. The company is a large enough midstream company that it’s able to do what several other companies do and can now increase margins with bolt-on acquisitions, primarily.

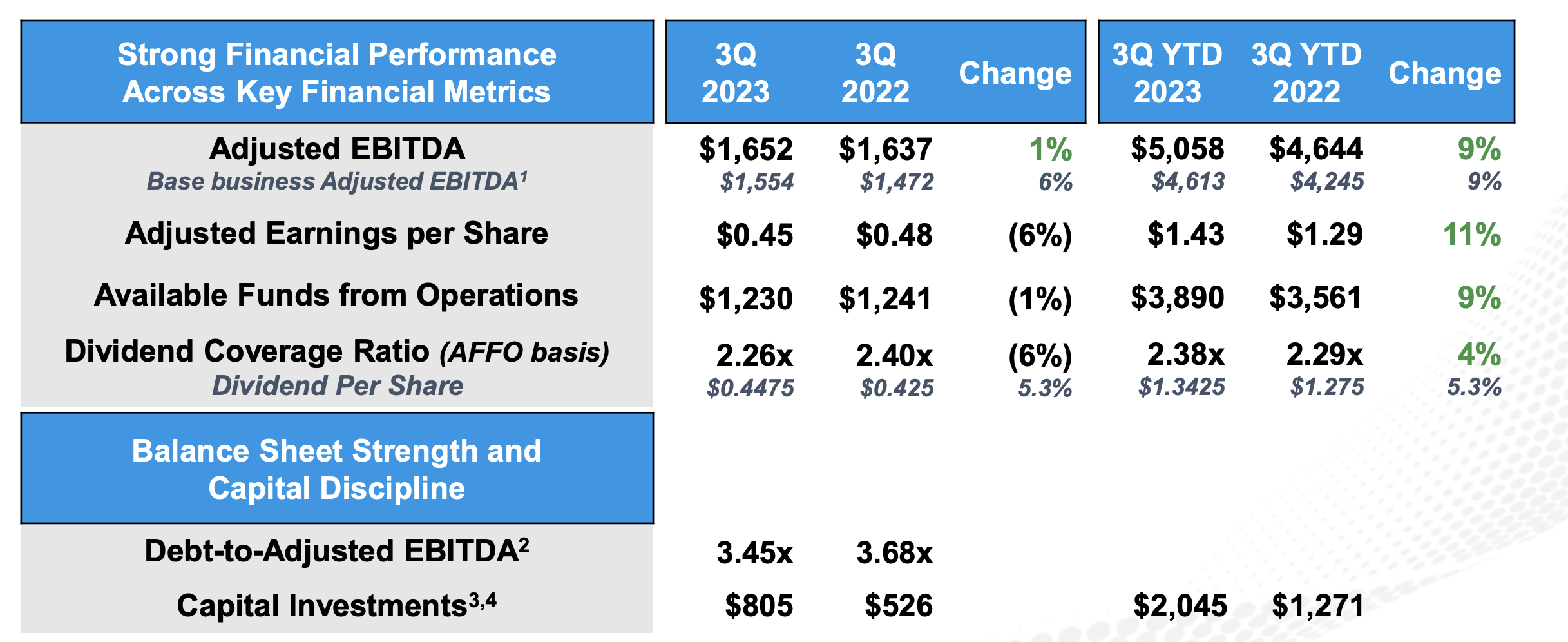

Financially, the company has increased its guidance and continued to perform well with its toll-road operator status. Despite an incredibly weak year for natural gas prices, the company’s performance here shows a continued ability to outperform.

Williams Companies Financial Performance

Diving into the details of the company’s financials, its EBITDA improved by 1% YoY and its EPS dropped by 6%.

Williams Companies Investor Presentation

Funds from operations dropped as well, along with dividend coverage. However, it’s worth noting that the drop in dividend coverage was due to an increase in the company’s dividend, with the company’s yield now crossing 5%. The company’s debt to adjusted EBITDA has declined as it’s paid down its debt, and it continues to invest heavily in its business.

Overall, the company’s financial performance has done well YoY. It’s also worth noting despite the comparable YoY performance, the company’s YTD performance has been much stronger than 2022, with a higher dividend coverage ratio despite a higher dividend as well.

Williams Companies Optimizations

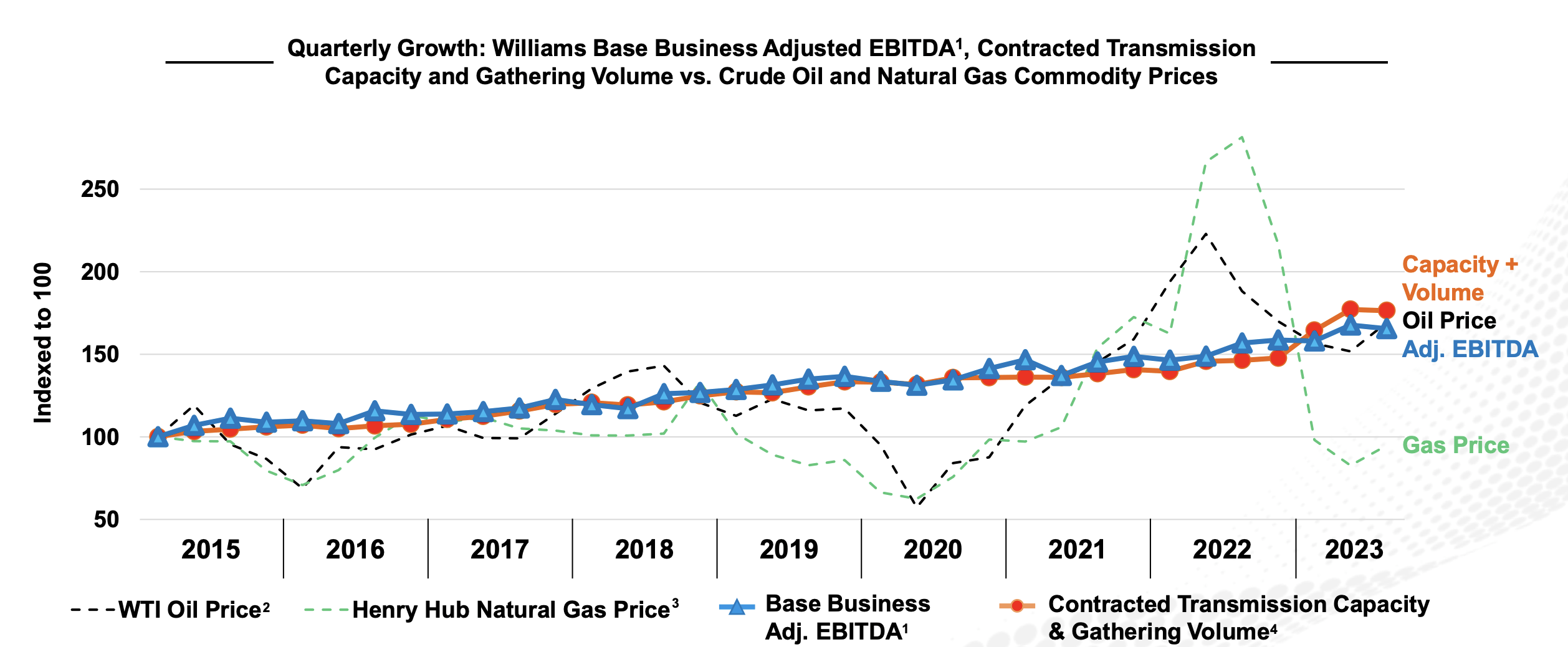

The company is working hard on continuing its growth despite volatility in natural gas prices.

Williams Companies Investor Presentation

31% of the company’s earnings continue to come from Transco, which is among the largest pipelines in the U.S., and one of the most important. The company has worked to be able to steadily increase capacity, and over the past 8 years, the company’s capacity has managed to increase by more than 50% throughout is system.

Part of this has been numerous bolt-on acquisitions. The company supplied 17.15 million dekatherm through Transco, and adjusted EBITDA has steadily increased despite substantial volatility in oil and natural gas prices. The company has been able to increase dividends and shareholder returns as a result of its reliability.

Thesis Risk

The largest risk to our thesis is continued long-term demand for the company’s assets. The company operates primarily the Transco pipeline along with associated pipelines, etc., all that are currently essential to our modern population; however, there’s no guarantee that natural gas will remain at the same demand in the coming decades.

That could substantially hurt future returns for shareholders.

Conclusion

The Williams Companies has an impressive portfolio of assets. The company is continuing to generate reliable cash flow and YTD its financials have improved dramatically. More importantly, the company has managed to provide reliable financial improvement despite operating in a market with incredibly volatile pricing, as it focuses on toll road pricing.

The company’s annualized FFO is more than $5 billion, versus a $40 billion market cap, giving the company a clear double-digit FFO yield. The company provides a dividend of more than 5% and has worked to improve its debt and overall shareholder returns. We expect the company to continue providing reliable shareholder returns going forward.

Overall, that makes the company a valuable investment.

Q2 2024 Earnings Call Transcript")