megaflopp/iStock via Getty Images

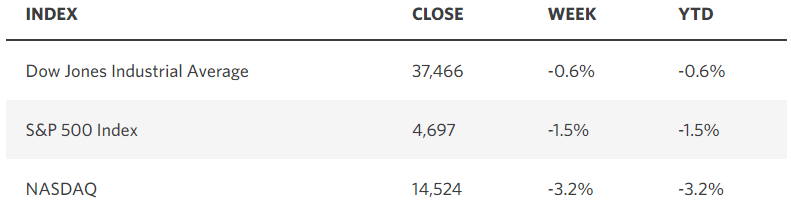

The weekly winning streak ended at nine, with stocks finally taking a breather to start 2024. I would not read anything more into last week’s decline than one step toward resolving an overbought condition. The indexes averaged a gain of 17% over the last nine weeks of the year, so we need to put the first four trading days of the new year into perspective. Regardless, those who think the outlook for a soft economic landing is suspect and disagree with the bull market narrative are bound to make a mountain out of a molehill. The rate of growth in most high-frequency economic indicators is scheduled to slow meaningfully year over year, as we feel the full impact of the Fed’s 11 rate hikes over the past 20 months. The focus on inflation will soon shift to economic growth and its sustainability. Again, this will fuel recession warnings. Therefore, we want to focus on the rate of change in leading indicators to be sure that the soft landing is on track. Last week’s jobs report for December is not on my list of indicators.

Edward Jones

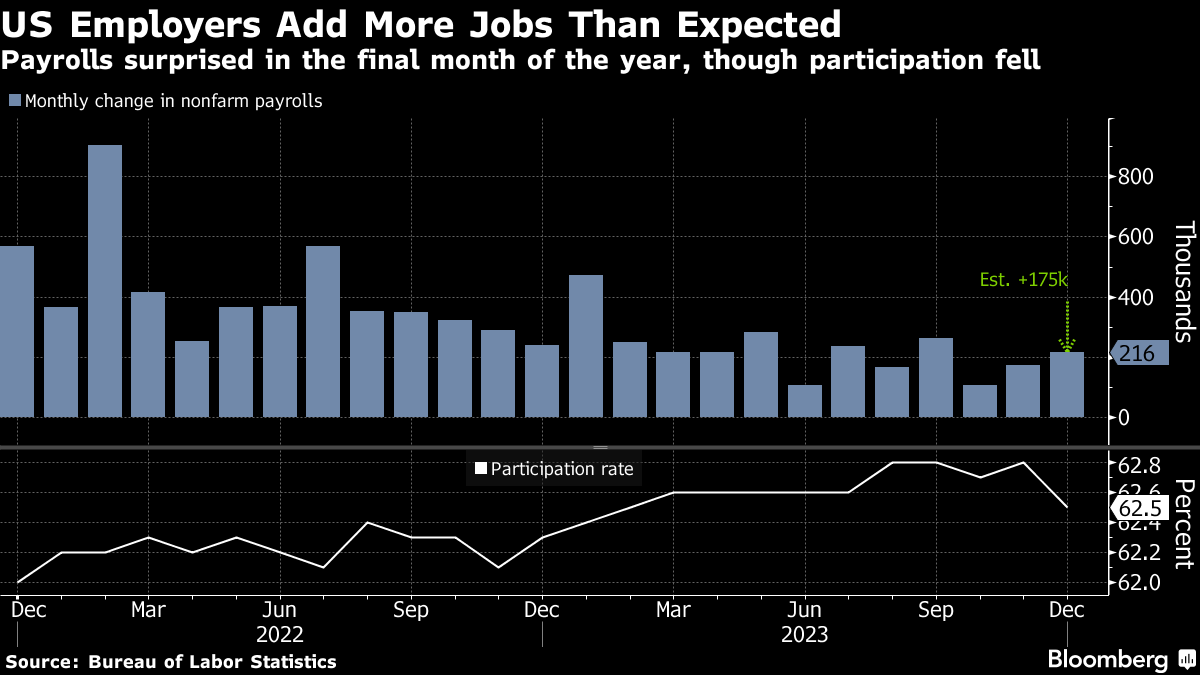

I have never understood why market pundits place so much importance on the estimate for how many jobs were created in the prior month when it comes to anticipating future monetary policy moves or the strength of the economy moving forward. All the jobs report does is reaffirm the trends already in place or confirm leading indicators that tell us a change in trend is at hand. The estimate of 216,000 jobs for December surpassed expectations of 175,00, but the prior two months were revised lower by a combined 71,000 for a net gain of just 145,000. Additionally, the participation rate fell from 62.7% to 62.5%. These numbers both reflect a continued softening of labor market conditions.

Bloomberg

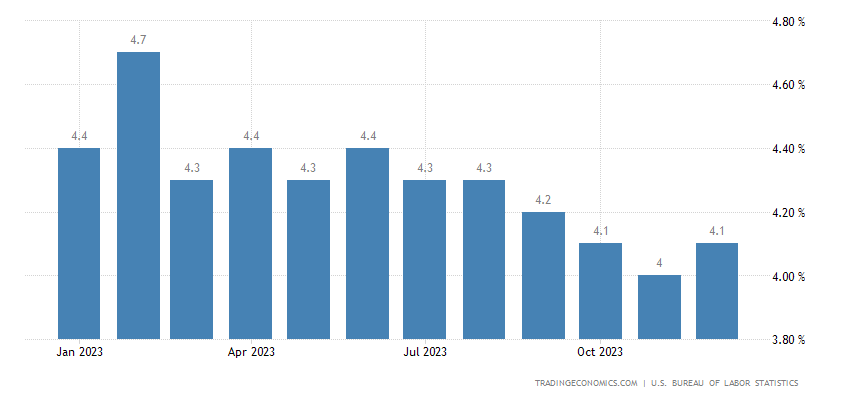

Wages rose during the month by a greater-than-expected 0.4%, which resulted in the annual rate of increase climbing from 4% to 4.1%. Some suggested that this may force the Fed to delay cutting rates in March. Why would the Fed use a lagging indicator to make a policy decision that has a tremendous lead time? The trend in wage growth continues to be gently lower, which is why we want to sustain real wage growth and keep inflation-adjusted consumer spending levels reflecting growth. There was no new news here.

Trading Economics

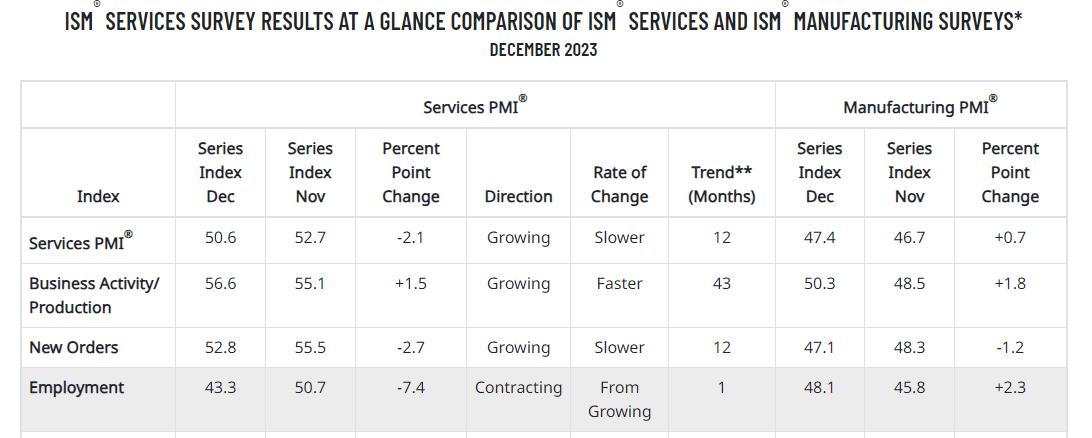

What I do consider to be a yellow flag is last week’s Purchasing Manager’s Index (PMI) for the service sector from the Institute for Supply Management. In the December survey, we saw the overall index fall from 52.6 to 50.6, which means we are dangerously close to falling below the line of demarcation between growth and contraction. In fact, the decline in new orders and a sharp drop in employment suggest a significant softening in activity is coming in January. For me to be more concerned, I need to see the same rates of change in the service sector index from S&P Global, which involves a different group of survey respondents.

ISM

This raises the bar of importance for the upcoming retail sales and personal spending reports, which need to continue growing on a real year-over-year basis for the soft landing to stay on track. It is a retrenchment in consumer spending that leads to job losses, which then results in less aggregate income, and in turn lower consumer spending levels. We must thread the needle this year in terms of realizing softer rates of economic growth that allow the Fed to reduce interest rates without leading to a contraction in economic activity. For now, it looks like we are still on track.

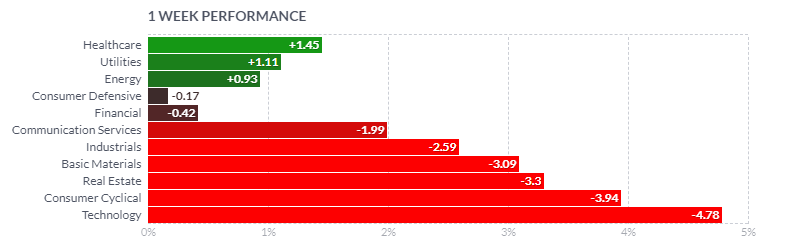

I read over the weekend that last week’s rotation out of 2023’s leading sectors and into its biggest losers was a foreboding sign. I could not disagree more. This is a part of the improvement in breadth, which typically leads to more broad market gains. Granted, the inflow was into defensive sectors of the market, but I think investors are looking for value after the long stretch of outperformance for growth.

Finviz

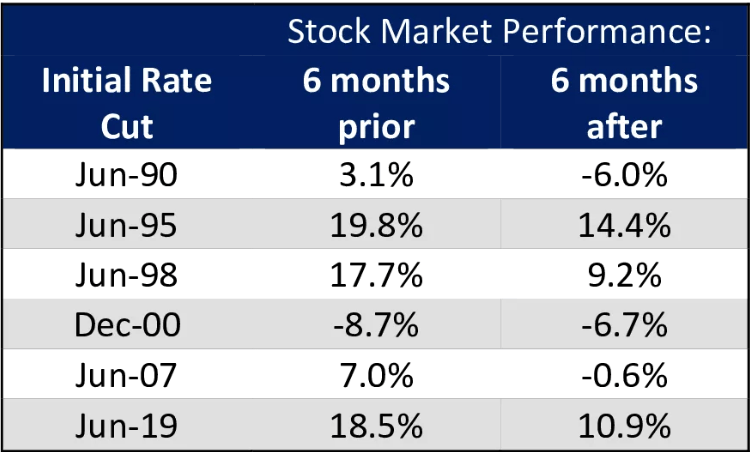

Additionally, provided we don’t see a recession this year, the period after a rate-cut cycle begins has been a tailwind for the stock market, as seen below. I think the closest comparison to current conditions is the 1995 mid-cycle slowdown. Therefore, let’s resolve this overbought condition and set the stage for a run at new all-time highs in the S&P 500, but with far broader participation than last year.

Edward Jones

Q2 2024 Earnings Call Transcript")