If your family is like mine, you kept Amazon (AMZN 0.46%) busy over the last few months. Rarely a day went by when we didn’t have at least one Amazon package at our doorsteps.

Amazon’s e-commerce unit has made the company a household name. The scale of its operations surpasses all others. So it would make sense if Amazon rakes in most of its profits from e-commerce. But it doesn’t. Nearly three-quarters — 74% — of its operating income comes from another source.

Image source: Amazon.

How Amazon makes money

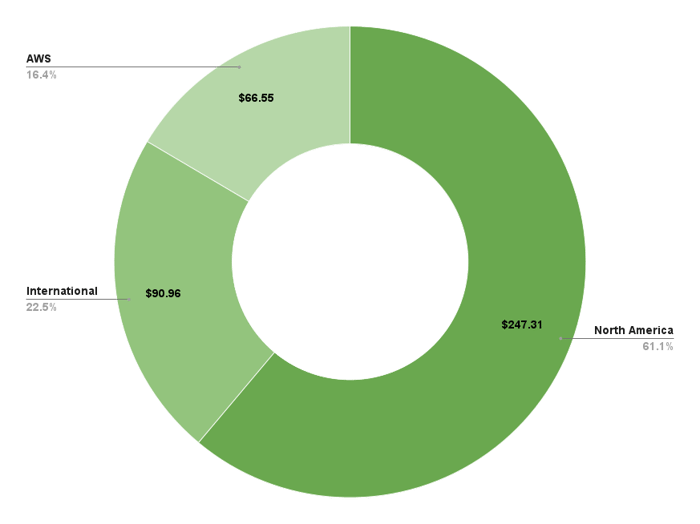

To be sure, Amazon’s e-commerce business generates the most revenue for the company. In the first nine months of 2023, Amazon’s net revenue totaled a little over $66.5 billion. The company’s North American and International segments, which focus primarily on e-commerce, together accounted for 83.6% of that revenue. Cloud platform Amazon Web Services (AWS) contributed the rest.

Data source: Amazon. Chart by author.

Granted, not all of the revenue in the North American and International segments comes from e-commerce. Amazon also operates some physical stores (including Whole Foods) and makes an increasing amount of money from advertising. However, the company’s online stores and third-party seller services, which fall squarely into the e-commerce category, rake in the lion’s share of the company’s total sales.

But it’s a completely different story when it comes to operating income. Amazon posted consolidated operating income of $23.6 billion in the first nine months of 2023. AWS contributed nearly $17.5 billion, or roughly 74%, of that total.

Why is AWS so profitable?

Operating income is sometimes referred to as operating profit. It measures the amount of money left over after subtracting operating expenses including the cost of goods sold (COGS) from revenue. It’s not the same as net profit (which also subtracts taxes and interest expense), but they’re closely related.

Why is AWS so profitable for Amazon? The cloud unit’s operating expenses as a percentage of net sales are much lower than the percentages for the company’s North America and International segments. That shouldn’t be surprising. The massive logistics network and infrastructure required to support Amazon’s e-commerce operations are expensive.

Of course, AWS’ operating costs aren’t insignificant. Amazon spends a lot of money on the cloud services unit’s technology infrastructure and the staff who run it.

Those costs could rise as Amazon invests more heavily in artificial intelligence apps and tools for AWS. CFO Brian Olsavsky noted in the company’s Q3 conference call that Amazon plans to increase its investments in generative AI and large language models, in particular. to “support the growth of our AWS business.” However, it’s a virtual certainty that AWS will continue to be Amazon’s biggest profit machine.

Great news for Amazon

Amazon’s e-commerce business still has plenty of room to grow. E-commerce made up only 15.6% of total U.S. retail sales in 2023 Q3. The market penetration is even lower in some parts of the world.

However, the great news for Amazon is the opportunity for AWS. The explosion in the use of generative AI last year likely only represents the tip of the iceberg. As progress is made toward achieving artificial general intelligence (AGI), the momentum for AI is likely to accelerate.

Amazon CEO Andy Jassy has said on several occasions that only 5% to 10% of global IT spending is currently in the cloud with most spending still on-premises. Jassy believes those numbers will flip over the next 10 to 15 years. If he’s right (and I suspect he is), AWS should be a huge winner from the trend.

Yes, AWS faces some strong rivals with their own impressive cloud platforms. Jassy, though, argued in the Q3 call that “customers want to bring the [AI] models to their data, not the other way around.” He quickly added, “And much of that data resides in AWS as the clear market segment leader in cloud infrastructure.”

The bottom line is that Amazon’s biggest growth driver is also its most profitable business, by far. That should bode well for the company’s long-term earnings outlook. And where earnings go, stock prices tend to follow.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Keith Speights has positions in Amazon. The Motley Fool has positions in and recommends Amazon. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")