imaginima

Dear readers,

Today, I would like to take a look at a self-storage REIT, Public Storage (NYSE:PSA), and why it might make a good investment. Self-storage REITs can benefit from two major demand shifters that we are seeing in the market right now.

1. Migration – which has been on the rise as many people move because of work. This often makes it harder for them to store their belongings which is why they opt for a self-storage unit.

2. Downsizing – since the price of living is increasing many people need to move to a smaller home to save some money. This makes self-storage REITs benefit yet again since people need someplace to put their things after moving to a smaller space.

Portfolio

They are the second biggest self-storage REIT, right after Extra Space Storage (EXR). They own nearly 3300 properties in 40 states covering 238 million rentable square feet. The company is the fastest growing among its competitors and is actively expanding its properties and it has grown its portfolio by 34% since 2019. This year they had 153 acquisitions totaling 11,296 thousand square feet, 6 new developments (595 thousand square feet), and 5 new expansions (326 thousand square feet).

At the moment, the industry is experiencing a decrease in demand, however, the occupancy gap for PSA has narrowed down from 250 basis points at the beginning of the year to 60 basis points in the last quarter. As stated in the Q3 earnings call this is thanks to a good mix of marketing, promotion, and rental rates indicating that the management is doing a good job in getting customers to choose PSA. They have also mentioned that while the demand from move-in customers has slowed down because of higher mortgage rates, they have seen far more new customers who are renters who still rent for longer periods of time.

Financials

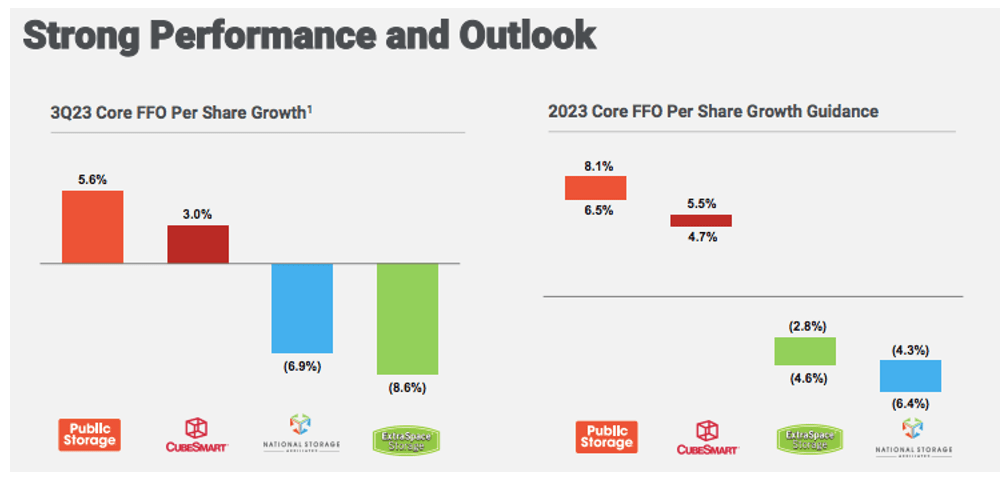

Now I want to take a closer look at their operational metrics. The core FFO stood at $4.33 in the last quarter and it has grown 5.6% year-over-year, mainly due to new acquisitions. Same-store revenues have increased by 2.5% quarter-over-quarter. Operating costs increased by 2.8% in the last quarter and NOI has grown by 2.4%. One thing that makes PSA stand out from its competitors is its industry-leading operating NOI margins of 80%. The company also has an initiative to raise the margins even further by operating model transformation and sustainability initiatives. More specifically payroll cost and utility cost savings.

The company has reviewed its guidance and expects even greater growth until the end of the year. The revenue growth is expected to be 4.4% at the midpoint (up from 4.1% from prior guidance), NOI growth is said to increase by 3.95% at the midpoint and expenses are supposed to increase a bit more slowly by 5.75% compared to prior guidance of 6.25% at the midpoint. The FFO is expected to grow by 7.3% at midpoint, which is the fastest growth among the competition.

PSA Presentation

Balance sheet

Their balance sheet is A-rated so it is one of the safest out there. They have $9.1 billion in debt majority of which is fixed. The blended rate is 2.9% and their debt to EBITDA ratio is 2.7x. So overall a very healthy balance sheet.

Dividend

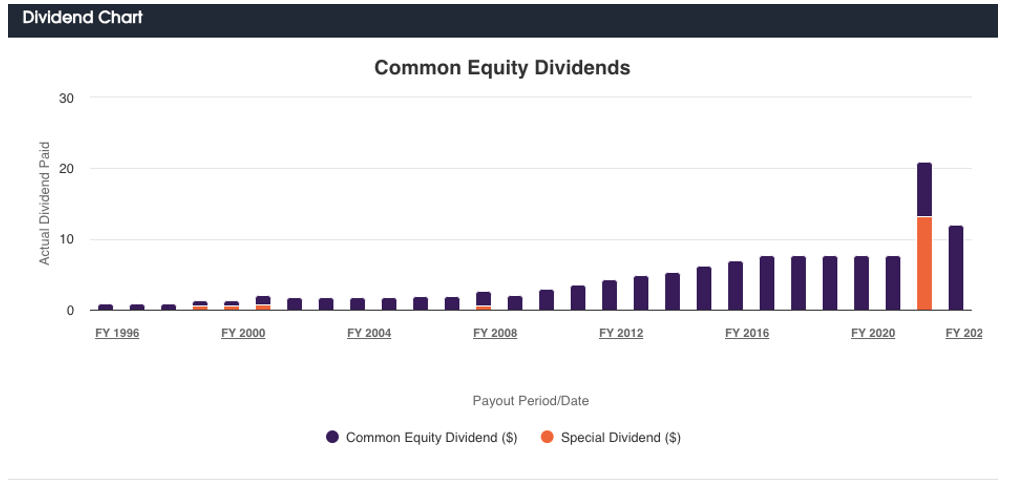

They currently pay a $12 annual dividend which translates to a 4% yield with a healthy payout ratio of 71%. Last year was the first year of dividend increases since 2016 and was accompanied by a juicy special dividend. This year the dividend has increased even further.

PSA Presentation

Before I get to the valuation, I would like to mention the main risk I see with this investment. In case of a recession people will want to cut their spending and since the rental contracts for self-storage units are short people might want to withdraw and save some money on this expense.

Valuation

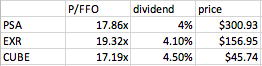

I would like to compare Public Storage with its main competitors EXR and CubeSmart (CUBE). One major advantage PSA has, which I have mentioned before, is their industry-leading margins which in my opinion would justify a premium in the P/FFO, yet they are trading just a bit above CUBE and much lower than EXR. They do have the lowest dividend yield but not by much and I do see potential upside in the stock beyond the dividend.

Compiled by the author

They have been doing a great job in expanding the company, dealing with lower occupancy levels, and based on the Q3 results and guidance for the rest of the year the operational metrics are strong. Besides that, they have a very healthy balance sheet which is why I expect them to grow.

For FFO growth I will assume the bottom of the guidance for the year of 6.5%. Which will leave us with an FFO of around $20 per share by the end of 2025. I would expect the P/FFO to return to around 20x (20.33x is the historical average) which combined with the FFO could result in a price of around $400. That would mean around 33% of upside. Combined with the dividend we could get a double-digit return of around 15% per year. This is a good enough return for me since I see the company as pretty low-risk. I therefore rate the company a BUY here at $300.19 per share.

Q2 2024 Earnings Call Transcript")